Total 2023 municipal bond volume fell slightly from 2022 as market volatility, higher interest rates, pandemic aid and slower economic growth kept issuers on the sidelines.

However, a robust fourth quarter buoyed issuance for the year, so volume only ticked down 2.8%, much better than previous quarters where issuance was down double digits.

The year ended on a positive note as December municipal bond issuance, at $23.842 billion, was up 17.6% year-over-year from $20.273 billion in 2022.

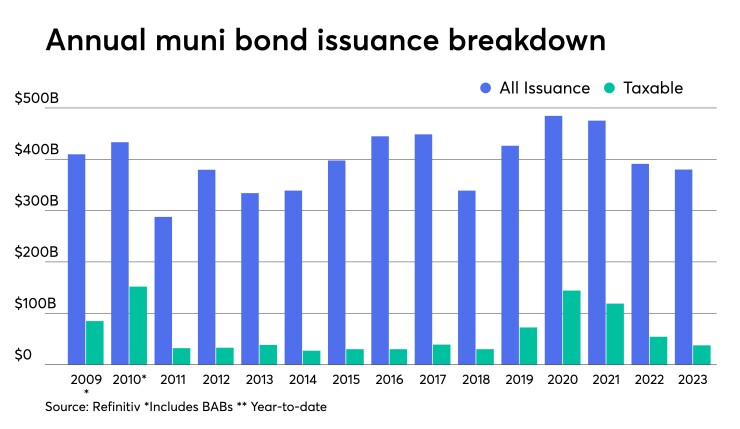

The muni market saw $379.992 billion of debt issued in 2023, only $11.076 billion less than the $391.068 billion seen in 2022. This is less severe than last year when issuance fell 19.1% from 2021.

Tax-exempt issuance rose 3.3% to $325.840 billion from $315.317 billion in 2022. Taxable issuance dropped 31% to $37.443 billion from $54.279 billion in 2022.

Refundings were up 1.5% to $50.777 billion from $50.003 billion in 2022. New-money volume dipped 4.9% to $294.558 billion from $309.853 billion in 2022.

Firms were mixed on

However, some firms

“I was definitely expecting lower issuance,” said Tom Kozlik, head of municipal research and analytics at HilltopSecurities Inc., of 2023’s issuance figure.

He initially predicted issuance would be $350 billion due to economic growth being forecasted to be lower than the year before and interest rates would be as high if not higher. He opted against revising his forecast lower mid-year.

The first quarter of this year, at $79.752 billion, was down 23% from Q1 2022 at $103.6 billion.

“At that point, folks were preparing for a scenario where growth was going to be substantially lower,” he said. “In some cases, they were expecting that there might be a recession.”

Issuers, he said, “were responding to a situation where they struggled to batten down the hatches for an economic situation like we saw 10-plus years ago.”

But by the middle to the end of the third quarter, the macroeconomic landscape improved and market participants believed a soft landing was possible, he said.

Then toward the end of the year, economic data came in that proved there would not be a recession in 2023, which “opened up” issuers to start selling debt, he said.

Volume surged 31.7% in the fourth quarter, rising to $99.339 billion in 2023 from $75.426 billion in 2022.

However, Vikram Rai, head of municipals market strategy at Wells Fargo, said the yearend volume total was not a surprise.

Rai, while head of Citi’s Municipal Strategy group, forecasted supply at $450 billion. He later revised his forecast to around $400 billion, which he said could be a “heavy lift,” before further revising his forecast downward to around $380 billion.

In 2023, he said “a confluence of inhibitors kept supply much lower than expected.”

First off, this year saw consistent yield volatility that kept municipal issuers on the sidelines and severely hindered refinancing volume,” he said.

There were also expectations of an impending rate rally.

Many issuers sat on the sidelines because yields were too high, prompting them to push deals in the pipelines to next year, he noted.

“Historically, rates have rallied once the Fed goes on ‘hold,'” he said. “While we are still uncertain if the Fed is truly ‘on hold,’ the belief among issuers that rates would rally led them to delay non-essential projects as they felt they could finance with better rates in a few weeks or months.”

Now that yields have rallied, things have worked out “very well” for those who waited and will now come to market in 2024, according to Rai.

Furthermore, many state and local governments had “built up significant cash piles owing to pandemic-related federal aid, and this had also reduced their need to tap capital markets.”

Kozlik said the slight decrease in volume was due to economic growth being a “little bit lower” and higher interest rates.

“When growth slows, state and local governments can’t deficit finance the way that the federal government does,” he said.

“At a time when growth is going to be lower, or there’s going to be a potential recession, it’s hard to think that issuers are going to start to increase their overall issuance activity,” he said. “Because they not going to and in some ways, they’re not able to put themselves in that situation.”

Going into 2024, most firms

The estimates for 2024 are based on a variety of factors, including municipalities exhausting pandemic-era government funds; pent-up demand and a backlog of projects; recession fears; Fed Reserve monetary policy; and the 2024 elections.

On the high end is Municipal Market Analytics Inc., which expects $425 billion to $450 billion and Wells Fargo at $425 billion. Those with lower forecasts include HilltopSecurities, which sees issuance coming in at $330 billion while Ramirez & Co. expects $375 billion.

For January, in particular, Rai — who expects issuance to be $425 billion in 2024 — said market participants are “desperately” waiting to see where issuance falls for the first month of the year.

The expectation is January will see an uptick in volume year-over-year as some deals earmarked for 2023 got pushed out to next year, he said.

There are already larger deals are set to come to market later that month. Jefferson County, Alabama, is set to price $2.5 billion of sewer revenue warrants during the second week of the month, and the New York State Thruway Authority is set to price $1.2 billion of general revenue bonds during the final week of January.

Furthermore, now that there is conviction among market participants that the Fed is holding rates steady and will start cutting next year, Rai expects to see supply ramp up in the first half of the year.

However, Kozlik believes issuance will fall to $330 billion in 2024. Growth will fall year-over-year, leading new-money issuance to drop. Meanwhile, interest rates, which potentially lower in 2024 than in 2023 but still “relatively high,” and the lack of refunding candidates will also lead refundings to fall.

The overall environment in 2024 will be closer to what the market saw in the first three to six months of 2023. If that doesn’t happen, Kozlik concedes issuance may be higher due to positive sentiment, though he does not see that happening from a macroeconomic perspective.

December issuance details

Tax-exempt issuance was up 33.9% to $21.232 billion in 405 issues in December from $15.857 billion in 416 issues in 2022.

Taxable issuance fell 5.3% to $1.946 billion in 41 issues from $2.055 billion in 54 issues a year ago. Alternative minimum tax issuance decreased 71.8% to $664.6 million from $2.36 billion.

New-money issuance ticked up 0.3% to $17.66 billion from $17.614 billion last year. Refundings surged 141.9% to $1.21 billion from $603.1 million.

Issuance of revenue bonds increased 10.5% to $16.133 billion from $14.601 billion in December 2022, and general obligation bond sales rose 35.9% to $7.71 billion from $5.672 billion in 2022.

Negotiated deal volume was up 38.3% to $17.216 billion from $12.449 billion a year prior. Competitive sales increased 56.1% to $5.228 billion from $3.349 billion in 2022.

Deals wrapped by bond insurance in December decreased 18.8% to $1.246 billion in 62 deals from $1.535 billion in 64 deals a year prior.

Bank-qualified issuance dropped to $386.5 million in 99 deals from $439.6 million in 96 deals in 2022, a 12.1% decrease.

In the states, Texas accounted for the most volume in 2023.

Issuers in the Lone Star State sold $59.013 billion, a 22.5% increase year-over-year. California was second with $53.938 billion, up 14.3% year-over-year, New York was third with $42.256 billion, down 15.4%. Illinois came in fourth with $14.314 billion, up 10.8%, and Florida rounds out the top five with $13.419 billion, a 16% decrease from 2021.

The rest of the top 10 are: Pennsylvania with $11.945 billion, down 0.9%; Washington with $9.332 billion, up 1.1%; Georgia with $9.262 billion, down 8.1%; Massachusetts at $8.649 billion, down 31.4%; and Michigan with $8.57 billion, a 2.4% decrease from 2022.