Municipals were steady Tuesday as the last week of the year got underway. U.S. Treasuries were little changed and equities ended up.

The two-year muni-to-Treasury ratio Tuesday was at 59%, the three-year at 59%, the five-year at 59%, the 10-year at 59% and the 30-year at 86%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 59%, the three-year at 59%, the five-year at 58%, the 10-year at 59% and the 30-year at 85% at 4 p.m.

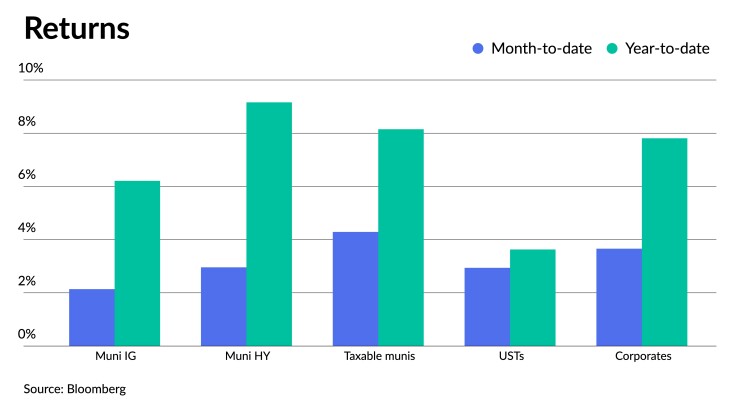

Munis’ strong performance from November continued into December, said Miguel Laranjeiro, a portfolio manager at abrdn.

Muni yields have fallen 29 to 35 basis points this month, according to Refinitiv MMD. The asset class is returning 2.14% month-to-date and 6.21% year-to-date. Volume is set to come in around $30 billion for the month, up from $20.1 billion in December 2022.

However, issuance in 2023 will be down year-over-year for the third straight year. Volume for the year was at $375.5 billion, as of Wednesday, and with issuance falling to a trickle this week, it will not surpass the $390.7 billion

“Issuers have been on the sidelines [this year] until they see some rate stability, so going into 2024, that stability should be more inviting for issuers to remarket and bring new money to the table,” Laranjeiro said. “It provides a more friendly environment for issuers to deploy capital.”

He expects a pickup in supply in 2024. This year, supply has been lackluster, especially compared to the five-year average.

Investor demand, he noted, may also pick up with it.

This year, the greatest demand has been from separately managed accounts and exchange-traded funds.

There have also been continuous outflows from muni mutual funds this year, albeit to a much lesser extent than last year, he said.

However,

This could continue in 2024.

While things could remain choppy in the first quarter of next year, as “we get to the second half or maybe even midyear of 2024, flows, especially in the mutual fund space, may start to turn around a little bit as munis provide an attractive relative value given the credit fundamentals in the asset class versus some of their corporate counterparts and where yields are at the moment,” Laranjeiro said.

For the upcoming year, the Fed will react to what happens in the labor market. “The consumer still looks strong, the labor markets still look strong,” he said.

At this point, Laranjeiro said yields are priced for an immediate recession.

“There’s more risk to the downside of long-end and even short-term yields than there is too to the upside,” he said.

He believes the market might have “gotten a little ahead of itself in pricing in a recession.”

Currently, the market is pricing in the Fed cutting rates in March, he said.

“So I’d be cautious at least on adding duration in the first quarter until we start seeing some weakening either from the labor market or from the retail consumer,” he said.

He believes the U.S. is about to enter a recession. During recessions, he said, munis usually benefit from the flight-to-quality trade.

“It remains a relatively attractive asset class if that is what winds up playing out in 2024,” he said.

Heading into next year, munis from a fundamental standpoint look relatively attractive, especially compared to the beginning of previous recessionary periods, he said.

Munis, he said, are better prepared for it in this environment.

States’ balance sheets are relatively robust, though he notes they are “probably a bit past its peak levels.”

From a credit perspective, Laranjeiro is optimistic about where issuers are on a historical basis.

Secondary trading

Delaware 5s of 2024 at 2.82% versus 3.04% on 12/8. NYC TFA 5s of 2024 at 2.76% versus 3.07% on 12/6. Nevada 5s of 2024 at 2.91%.

DASNY 5s of 2025 at 2.77%. Santa Clara County, California, 5s of 2025 at 2.45% versus 2.49% Wednesday. University of California 5s of 2026 at 2.33% versus 2.37% Wednesday.

Washington 5s of 2029 at 2.32% versus 2.39% on 12/14. DASNY 5s of 2032 at 2.35% versus 2.35% Friday and 2.40%-2.34% Thursday.

NYC TFA 5s of 2039 at 2.93% versus 3.03% on 12/15 and 3.11% on 12/14. Ohio Water Development Authority 5s of 2041 at 3.03%-3.02%.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 2.69% and 2.54% in two years. The five-year was at 2.28%, the 10-year at 2.28% and the 30-year at 3.47% at 3 p.m.

The ICE AAA yield curve was bumped up to a basis point: 2.74% (unch) in 2024 and 2.55% (unch) in 2025. The five-year was at 2.27% (unch), the 10-year was at 2.31% (-1) and the 30-year was at 3.45% (-1) at 4 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 2.68% in 2024 and 2.55% in 2025. The five-year was at 2.31%, the 10-year was at 2.34% and the 30-year yield was at 3.43%, according to a 3 p.m. read.

Bloomberg BVAL was unchanged: 2.58% in 2024 and 2.49% in 2025. The five-year at 2.20%, the 10-year at 2.27% and the 30-year at 3.36% at 4 p.m.

Treasuries were little changed.

The two-year UST was yielding 4.347% (+1), the three-year was at 4.057% (+1), the five-year at 3.883% (flat), the 10-year at 3.892% (-1), the 20-year at 4.203% (-1) and the 30-year Treasury was yielding 4.044% (-1) near the close.