Municipals were a touch weaker outside of 15 years Wednesday as U.S. Treasury yields rose after the Federal Open Market Committee minutes were released but pared back losses as the afternoon progressed and were back at Tuesday’s levels near the close.

The tapering conversation continues, but Federal Reserve Board Chair Jerome Powell said the FOMC has made no decisions on timing.

Municipals largely sat on the sidelines as trading was light and few new-issues priced. Shorter trades did show firmer prints while out longer, they were mixed but long benchmark yields rose a basis point or two.

The massive summer reinvestments continue and are both sustaining the strength of investor demand and solidifying the technical footing of the market.

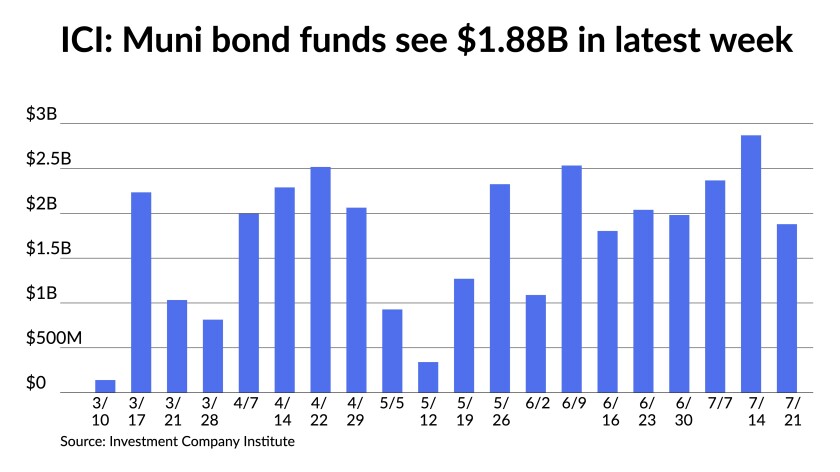

The Investment Company Institute reported another week of inflows, $1.879 billion for the week ending July 21, down from $2.879 billion the week prior, but still a strong showing for the fund complex that hit its 20th consecutive week of inflows.

Exchange-traded funds saw $458 million of inflows versus $562 million the week before.

Total assets held now total $57.3 billion year-to-date, according to ICI.

Separately, while the bipartisan group of senators in Washington reached an agreement on a $500 billion-plus infrastructure plan to be voted on as soon as Wednesday evening, it lacked any of the municipal market’s desired bond programs, such as direct-pay taxable bonds or tax-exempt advanced refundings.

Sources say they were stripped from the compromise deal and would likely be put into the larger tax and social spending package Democrats hope to get through Congress later this year.

Getting these deals done still face hurdles and much remains uncertain. Often municipal provisions are overlooked or tabled in last-minute negotiations.

As many issuers await more details from Washington on infrastructure, some participants say they are holding off on major investments and issuing new-money as a result. Visible supply is a mere $8.4 billion, according to Bond Buyer data, making for $25 billion of net negative supply, according to Bloomberg data.

Few new deals priced on FOMC day. Wells Fargo bought $112.345 million of hospital revenue bonds from the Iowa Board of Regents (Aa2/AA//). Bonds in 2021 with a 5% coupon yield 0.06%, 5s of 2022 at 0.09%, 5s of 2026 at 0.47%, 3s of 2031 at 1.13%, 2s of 2036 at 1.93%, 2s of 2041 at 1.93%, 2.25s of 2046 at 2.08% and 2.25s of 2051 at 2.34%.

Wells also bought $76 million of revenue bonds from Loudoun County, Virginia Sanitation Authority (Aaa/AAA/AAA/). Bonds in 2022 with a 5% coupon yield 0.06%, 5s of 2026 at 0.31%, 5s of 2031 at 0.79%, 1.75s of 2036 at 1.80%, 2s of 2041 at par and 2s of 2043 at 2.10%.

R.W. Baird bought $93 million of limited tax general obligation bonds from Fort Smith School District #100, Arkansas. Bonds in 2023 with a 2% coupon yield 0.35%, 1s of 2026 at 0.90%, at par at 1.65% in 2031, 2.20% in 2036, 2.65% in 2041, 2.90% in 2046 and 3% in 2049.

Municipal-to-UST ratios hovered at recent percentages and were at 65% for the 10-year and the 30-year was at 72%, according to Refinitiv MMD. ICE Data Services had the 10-year muni-to-Treasury ratio at 66% and the 30-year at 71%.

The market awaits bellwether Washington (Aaa/AA+/AA+/), which will sell $316 million of general obligation bonds at 10:30 a.m. eastern and $282 million of GOs at 11 a.m. eastern Thursday.

The state has tightened, along with most high-grade credits, since its last deal in April. When the state sold on April 20 they came at +2 basis points in 5 years, +7 in 10 years, +10 in 15 years, and +15 in 20-25 years, according to Refinitiv MMD. Washington is currently spread to MMD at +3 in 5 years, +7 in 10 years, +9 in 15 years and +10 basis points beyond that.

A block of Washington 5s of 2030 traded Wednesday at 0.80% (+4 MMD).

Secondary trading and scales

Trading was light with some firmer trades. Virginia College Building Authority 5s of 2022 at 0.06%. Georgia 5s of 2022 at 0.05%. District of Columbia 5s of 2022 at 0.05%. Delaware 5s of 2023 at 0.05%.

Prince George’s County, Maryland 5s of 2025 at 0.20%. North Carolina 5s of 2026 at 0.35%-0.34%. New York City Transitional Finance Authority 5s of 2026 at 0.39%-0.38%. King County, Washington 3s of 2027 at 0.53% versus 0.57% Thursday. Virginia 4s of 2028 at 0.57% versus 0.61% Monday. Florida Board of Education PECO 5s of 2031 at 0.86%-0.84% versus 0.89% Tuesday.

Austin, Texas ISD 4s of 2036 at 1.23%-1.22% versus 1.25% original. Massachusetts clean water 5s of 2038 at 1.02%-1.08%. Los Angeles Department of Water and Power 5s of 2039 at 1.18%-1.17%. Energy Northwest 5s of 2040 at 1.29%.

According to Refinitiv MMD, yields were steady at 0.05% in 2022 and at 0.06% in 2023. The yield on the 10-year sat at 0.82% while the yield on the 30-year rose two to 1.37%.

ICE municipal yield curve saw the one-year steady at 0.05% in 2022 and steady at 0.06% in 2023. The 10-year maturity at 0.84% and the 30-year yield rose one basis point to 1.36%.

The IHS Markit municipal analytics curve saw the one-year steady at 0.05% and the two-year at 0.06%, with the 10-year steady at 0.82%, and the 30-year yield at 1.36%, up one.

Bloomberg BVAL saw levels 0.04% in 2022 and at 0.04% in 2023, both steady, while the 10-year sat at 0.82% and the 30-year rose one to 1.35%.

Treasuries rose slightly while equities were mixed. The 10-year Treasury was yielding 1.233% and the 30-year Treasury was yielding 1.890% in late trading. The Dow Jones Industrial Average lost 89 points or 0.26%, the S&P 500 rose 0.14% while the Nasdaq fell 0.15%.

Informa: Money market muni funds fall $1.08B

Tax-exempt municipal money market fund assets fell by $1.08 billion, lowering their total to $91.90 billion for the week ending July 27, according to the Money Fund Report, a publication of Informa Financial Intelligence.

The average seven-day simple yield for the 157 tax-free and municipal money-market funds remained at 0.01% from the previous week.

Taxable money-fund assets rose by $45.40 billion in the week ended July 27, bringing total net assets to $4.352 trillion. The average, seven-day simple yield for the 763 taxable reporting funds remained at 0.01% from the prior week.

No clarity on tapering

The tapering conversation continues, but Federal Reserve Board Chair Jerome Powell called the FOMC’s discussion at this meeting “the first deep dive” on the pace and composition of the purchases.

“The Fed took another small step forward in their patient and methodical path towards tapering of their bond buying program,” said Jason England, global bonds portfolio manager at Janus Henderson Investors. With talk of progress toward its dual mandate and vows to provide advance notice of tapering, Janus maintains “tapering won’t begin until early next year.”

“Given the chorus of pricing pressures announced this earnings season and as employers continue to struggle in finding talent, mission accomplished still seems to be in the distant future,” said Ed Moya senior market analyst for the Americas at OANDA.

“Uncertainty for the Fed’s baseline to the outlook should solidify a dovish stance that could make the earliest for a taper announcement to be in September,” he said, echoing comments make earlier in a Bond Buyer podcast.

Members have “a range of views on timing,” Powell said. When asked, Powell said, he doesn’t expect an emphasis on cutting mortgage-backed purchases quicker than Treasuries. He also wouldn’t comment on the possibility of a statement being made during the Jackson Hole summit.

“Progress,” but not “substantial further progress” has been made toward the Federal Reserve’s dual mandate, according to the post-meeting statement, suggesting the panel is getting closer to tapering. In his press conference, Powell said, “the labor market still has a ways to go,” noting the high number of Americans without jobs and the low participation rate.

In its post-meeting statement, the FOMC noted its December commitment to buy $80 billion of Treasury securities and $40 billion of agency mortgage‑backed securities until “until substantial further progress has been made toward its maximum employment and price stability goals.” The statement continues: “Since then, the economy has made progress toward these goals,” and the panel will continue to assess progress at future meetings.

“I think that was a big change,” said Tom Porcelli, managing director and chief U.S. economist at RBC Capital Markets. “It is the Fed teeing up tapering.”

The change is “another incremental step toward tapering,” said Gary Pzegeo, head of fixed income at CIBC Private Wealth, U.S. “If markets accept the tweak in the Fed’s statement we could see them announce a schedule of tapered asset purchasing later in the year.”

The panel also held interest rates at the zero-lower bound. There were no dissenting votes.

Pointing to noticeable increases in inflation, the chair said above 2% numbers will increase for some more months as a result of unresolved bottlenecks. He said he considers these rises transitory because they are “not broad-based across the economy.” The increases mostly the result of jumps in certain categories that “won’t go on indefinitely.

The near-term inflationary risks are probably to the upside, he said, although he doesn’t expect the Delta variant to greatly impact the economy, as each time a variant arose, the economic impact was less than earlier hits.

“We’re already seeing significant inflationary pressures throughout the economy,” said Gary Zimmerman, CEO of MaxMyInterest. “While the Fed must walk a careful line between sustaining an economic recovery and avoiding runaway inflation, the fiscal stimulus planned by the federal government should pave the way for the Fed to begin paring back its dovish monetary policy.”

“I expect Chairman Powell will condition the market to expect an acceleration of the Fed’s plan to taper asset purchases, affording the Fed the flexibility to implement rate increases earlier in 2022 than had been previously articulated,” he said, expanding on his thoughts in a commentary.

As for rate hikes, Powell told reporters, that’s “not on our radar screen now.”

Wage hikes are not troubling, since it’s the lowest-paid workers who are making the biggest gains and these are not showing up in unit labor costs, Powell said.

Powell often deferred questions, such as timing of taper and the definition of substantial further progress, by saying that needs to be a panel decision, not his alone.

“He is trying to strike the right balance between what he thinks and the thoughts of his colleagues,” said RBC’s Porcelli. “But clearly, he is on one side and multiple of his colleagues are on the other side.”