Municipal bonds rallied Wednesday as triple-A benchmark yields fell as much as five basis points out long but bumps were seen across the curve, moving levels on high-grades below 1% on bonds maturing inside 14 years, while another round of billion-plus inflows were reported.

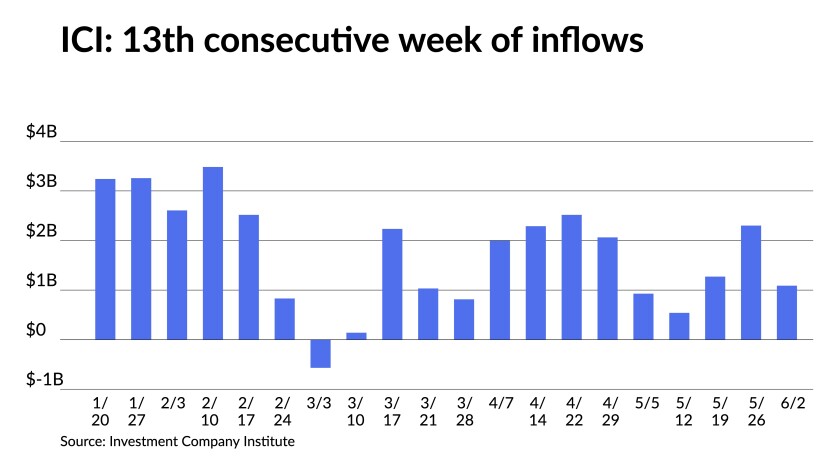

The Investment Company Institute reported $1.089 billion of inflows into municipal bond mutual funds for the week ending June 2 after $2.325 billion reported the week prior. Exchanged traded funds saw $286 million of inflows after $285 million the week before.

Solid secondary trading pushed levels lower from the start and new-issues were strongly bid in the competitive space — yields bought through triple-As and short coupons abound outside 10 years — and negotiated deals repriced to lower yields — West Virginia saw up to 15 basis point bumps.

U.S. Treasuries made gains ahead of Thursday’s jobless claims and CPI data. The 10-year U.S. Treasury was yielding 1.49% near the close The municipal 10-year landed at 0.89% on several scales, last below 0.90% in February prior to the sell-off that month. The 10-year opened 2021 at 0.67% while the 10-year UST started off the new year at 0.91%.

The municipal to UST ratios hovered around recent percentages, dipping lower on the long bond once again. The 10-year closed at 60% and at 64% in 30-years, according to Refinitiv MMD. ICE Data Services saw ratios on the 10-year at 59% and the 30-year at 65%.

The tightening spreads between triple-A and double-A municipal bonds is dramatic inside 10 years, notes FHN Financial’s Kim Olsan.

She pointed to new-issues on Tuesday, including Aa2/AA-rated Indiana Finance CWA Water Authority bonds were done +6/AAA in the 5-year maturity; Wisconsin’s GO sale (Aa1/AA) came with a 7-year yield of 0.69%, or a mere +1/AAA spread.

In pricing Wednesday, those levels tightened further on new issues. Los Angeles Department of Water and Power (Aa2//AA-/AA) saw its 5-year with a 4% coupon yield 0.41% +1/AAA, West Virginia parkway authority (/AA-/AA-/) 5-year with a 5% coupon yield 0.44% +4/AAA, Fort Worth Texas 4s of 2026 yield 0.44% +4/AAA.

Gilt-edged Arlington County, Virginia 5s of 2026 were bought at 0.41% in the morning competitively.

“The spread compression (moving ratios into the 50% range) is likely due in part to the expected mismatch of issuance and redemptions, estimated by some analysts at more than $50 billion between now and August,” Olsan said. “Of course, just how much under-served demand surfaces depends on most of the reinvestment flow cycling back into the market. One headwind that could develop is if marginal tax-bracket buyers (those below the top rate) are diverted into other assets on the richness of munis.”

In the primary, RBC Capital Markets priced for retail investors $439.4 million of power system revenue refunding bonds for the Department of Water and Power of the City of Los Angeles (Aa2//AA-/AA). Bonds in 2022 with a 3% coupon yield 0.07%, 4s of 2026 at 0.41%, 5s of 2031 at 0.93%, 5s of 2036 at 1.14%, 5s of 2041 at 1.34%, 5s of 2046 at 1.48% and 5s of 2051 at 1.53%.

Secondary trading of the issuer showed strong prints, especially out long, as it was pricing bonds in the primary.

Los Angeles Department of Water and Power 5s of 2040 at 1.21%-1.20% versus 1.27%-1.26% Tuesday. LA DWP 5s of 2046 at 1.38% versus 1.44%-1.43% Tuesday and 1.48%-1.57% Friday. LA DWP 5s of 2050 at 1.42% versus 1.45% Tuesday. LA DWP 5s of 2051 at 1.44% versus 1.51% Tuesday and 1.55% Friday.

If those trades and the moves on Wednesday were any indication, pricing for institutions should see this deal with much lower yields.

Wells Fargo Securities repriced with four to 14 basis point bumps $333.6 million of senior lien turnpike toll revenue bonds for the West Virginia Parkways Authority (/AA-/AA-/). Bonds in 2022 with a 5% coupon yield 0.06% (-4), 5s of 2026 at 0.44% (-11), 5s of 2031 at 1.03% (-14), 5s of 2036 at 1.25% (-10), 3s of 2041 at 1.78% (-7), 5s of 2047 at 1.56% (-12) and 4s of 2051 at 1.74% (-10).

In the competitive market, Fort Worth, Texas sold $157.215 million of water and sewer revenue refunding bonds (/AA+//) to Citigroup Global Markets Inc. Bonds in 2022 with a 2% coupon yield 0.06%, 4s of 2026 at 0.42%, 4s of 2031 at 1.02%, 2s of 2036 at 1.75%, 2s of 2041 at 1.95%, 2.125s of 2046 at 2.19% and 2.25s of 2051 at 2.25%, callable in 2/15/2030.

Fort Worth, Texas also sold $143.98 million of limited tax general obligation bonds (/AA/AA/AAA) to Morgan Stanley & Co. LLC. Bonds in 2022 with a 5% coupon yield 0.05%, 5s of 2026 at 0.45%, 4s of 2031 at 1.07%, 2s of 2036 at 1.81% and 2s of 2041 at 2.01%, callable in 3/1/2030.

Arlington County, Virginia (Aaa/AAA/AAA/) sold $95.7 million of general obligation bonds to J.P. Morgan Securities LLC with 5s of 2022 at 0.06%, 5s of 2026 at 0.41%, 5s of 2031 at 0.92%, 5s of 2036 at 1.07%, 5s of 2041 at 1.25% and 5s of 2046 at 1.39%.

Secondary trading and scales

Wisconsin 5s of 2022 traded at 0.05%. California 5s of 2025 at 0.24%. North Carolina 5s of 2026 at 0.40%. Fairfax County, Virginia 4s of 2026 at 0.45%. Fairfax County 4s of 2027 at 0.58%. Georgia 5s of 2028 at 0.64%.

Arlington, Texas ISD 5s of 2029 at 0.85%-0.82%. Vermont 5s of 2029 at 0.79%. Georgia 5s of 2029 at 0.76%. Georgia 5s of 2032 at 0.83%.

New York City 5s of 2032 at 1.16% versus 1.28% on May 27.

Seattle 4s of 2033 at 1.12%-1.11% versus 1.16% original.

Maryland 5s of 2033 traded at 1.00% in large $5 million-plus blocks versus 1.02% Tuesday.

Hawaii 5s of 2035 at 1.18%. Fairfax County water and sewer 5s of 2036 at 1.10% versus 1.30% on May 14.

San Antonio Texas ISD 4s of 2038 at 1.30%. Massachusetts clean water 5s of 2038 at 1.18%-1.17%.

University of Washington 4s of 2051 at 1.67%-1.65%.

Triborough Bridge and Tunnel 5s of 2056 traded at 1.69%.

High-grade municipals were better by two to five basis points, according to Refinitiv MMD’s AAA. Short yields were steady in 2021 and 2022 at 0.06% and 0.09%, respectively. The yield on the 10-year fell five to 0.89% while the yield on the 30-year fell five basis points to 1.39%

The ICE AAA municipal yield curve showed short maturities steady in 2021 at 0.05% and 0.09% in 2023. The 10-year maturity dipped four basis points to 0.89% and the 30-year yield fell five to 1.41%.

The IHS Markit municipal analytics AAA curve showed short yields fall one basis point to 0.06% and 0.09% in 2021 and 2022, respectively, with the 10-year down three to 0.89% and the 30-year yield down five to 1.43%.

The BVAL AAA curve showed the yield on the 2021 maturity at 0.05% and the 2022 maturity at 0.07%, both down one, while the 10-year fell four basis points to 0.87% and the 30-year fell four to 1.42%

In late trading, the 10-year Treasury was yielding 1.53% and the 30-year Treasury was yielding 2.17% while equities lost ground on the day with the Dow falling 138 points, the S&P 500 lost 0.16% and the Nasdaq fell 0.12%.

Informa: Money market muni funds rise $992M

Tax-exempt municipal money market fund assets rose $992.3 million, bringing total net assets to $93.40 billion in the week ended June 7, according to the Money Fund Report, a publication of Informa Financial Intelligence.

The average seven-day simple yield for the 162 tax-free and municipal money-market funds remained at 0.01% from the previous week.

Taxable money-fund assets increased $1.83 billion in the week ended June 8, bringing total net assets to $4.462 trillion.

The average, seven-day simple yield for the 761 taxable reporting funds remained at 0.01% from the prior week.

Overall, the combined total net assets of the 923 reporting money funds rose $2.83 billion in the week ended June 8.

Wednesday’s economic indicators

Wholesale inventories rose 0.8% to $698.0 billion in April, the Commerce Department reported. Compared to April 2020, inventories were 5.2% higher.

Economists surveyed by IFR Markets had expected inventories to have risen 0.8% in April after a similar 0.8% gain in March.

Wholesale sales also rose 0.8% in April, to $570.8 billion, after rising a revised 4.3% in March, originally reported as a 4.6% increase.

The April inventories to sales ratio remained at 1.22. The ratio in April 2020 was 1.67.