When the full Indianapolis City-County Council on Dec. 4 approved a plan to finance Eleven Park, a $1.5 billion mixed-use development anchored by a minor-league soccer stadium, the vote was nearly unanimous.

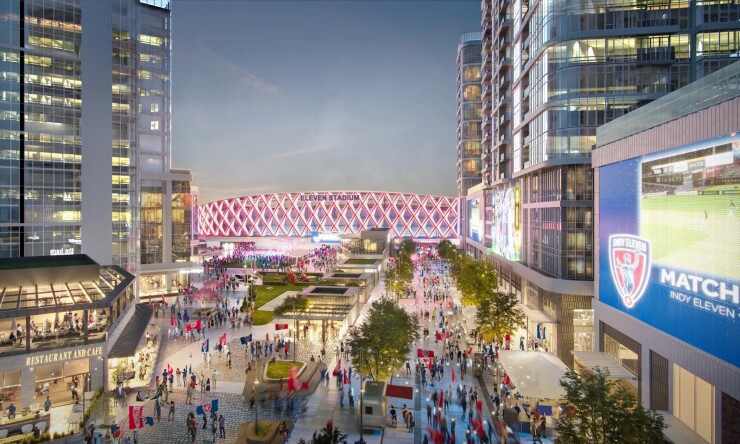

The plan, authorized by Indiana’s General Assembly, carves out a new tax area downtown: the Additional Professional Sports Development Area. It will enable the construction of a new soccer stadium surrounded by 197,000 square feet of stores and restaurants, 600 apartments, 205,000 square feet of offices, at least one hotel, an amphitheater and a concert hall.

The 20,000-seat soccer-focused stadium will be home to the Indy Eleven, which plays in the USL Championship, considered a Division II league by the U.S Soccer Federation, a step below Division I Major League Soccer.

Indy Eleven

The developer, Keystone Group, will chip in roughly 20% of the project’s overall cost, or around $300 million. State tax revenues will cover up to $9.5 million more. Beyond state retail and income taxes, local taxpayers will also contribute to the stadium through income taxes, food and beverage taxes within the PSDA and possibly innkeepers and admissions taxes.

The remaining costs will be financed through bonds issued by the Indianapolis Local Public Improvement Bond Bank. Its executive director and general counsel, Joe Glass, told The Bond Buyer that taxpayers’ contribution to the PSDA and the subsequent bond issuance “would apply specifically to the soccer stadium once a final deal is reached.”

The amount of bond proceeds going toward the project will hinge on a comparison of projected PSDA revenues to the financing costs of the bonds, according to

The PSDA will sit along the White River, on the south side of downtown, bounded by Washington St. to the north and I-70 to the south. The taxing district includes the site of the former Diamond Chain Manufacturing Co. headquarters — abandoned when that company moved operations to Fulton, Illinois — a property that Keystone President and CEO Ersal Ozdemir bought in October 2021, according to the

Despite the overwhelming City-County Council vote, public support for the project has been mixed.

In 2019, the Sports Innovation Institute at Indiana University-Purdue University Indianapolis

“Along generational lines, Millennials clearly showed the strongest support for a soccer stadium, followed distantly by Boomers and Gen X,” the institute noted.

Even with Millennial support, the new Indy Eleven stadium still placed last among other local venues in support for taxpayer funding of pro sports arenas.

In 2023, the Eleven averaged 9,709 fans for their home games at the 12,000-seat Carroll Stadium on the campus of Indiana University – Purdue University Indianapolis, according

At the Dec. 4 City-County Council meeting, only Councilor Ethan Evans voted ‘no’ on the PSDA. He chose not to run for re-election in 2023. Evans did not respond to requests for comment.

Economists have found limited economic benefits to municipalities from sports stadiums. In 2019, the

The journal cited research by Roger Noll and Andrew Zimbalist which found that new sports venues have

“Over the last thirty years, building sports stadiums has served as a profitable undertaking for large sports teams, at the expense of the general public,” the journal observed. “[These projects] can be an obstacle to real development in local neighborhoods.”

Noll, a professor of economics emeritus at Stanford University, said there have been “no significant changes” to the conclusions he and Zimbalist reached in the late 1990s. He said other potential economic benefits from stadiums have since been examined — an increase in property values; a rise in tourism; more businesses opening in the area — with the same results: usually zero benefit, and never enough of a positive impact to justify the public subsidy.

“Sports facilities have grown much more complex and expensive,” he added. “The present model design is to embed the facility in a much broader local economic development project … The other ancillary developments (residential, retail, entertainment) sometimes are successful, but the incremental value of the sports component is still small and less than the subsidy. [And] the more comprehensive development projects tend to cost more and involve larger public subsidies.”

Impact studies from developers often exaggerate the benefits of these projects, Noll said, but they tend to persuade people who are not fans of the team to support the project. As for opponents of such projects, they seldom triumph over developers — unless the matter is decided directly by voters, as it was recently in Tempe, Arizona, where voters in May

“Campaign expenditures in favor of the facility typically dwarf expenditures by opponents,” Noll said.

Bloomberg News

That dynamic is now playing out in cities across the country. Last year, at least a dozen professional sports teams — mainly National Football League and Major League Baseball teams — struck deals for new or renovated stadiums, according

In such deals, the financial interests of local communities sometimes clash with the interests of sports team owners, including in Indiana’s neighbor Illinois.

There the Chicago suburb of Arlington Heights, population roughly 75,000, is still wrestling with the prospect of hosting the Chicago Bears, looking to leave its

In Pawtucket, Rhode Island, another USL Championship stadium project has experienced a bumpy ride. According to the Providence Journal, municipal adviser Hilltop Securities resigned this August over the terms of a bond offering for a local soccer stadium project, Tidewater Landing. The Pawtucket redevelopment agency marketed

A local online news site obtained Hilltop’s

“Analyses using the consultant’s model projected net positive returns from the substantial public investments, which justified the funding decisions of the approving municipal bodies,” the economists wrote. But “analyses derived from the presented pro forma model do not provide credible evidence that these or other stadium developments are expected to produce economic benefits… Policymakers should remain skeptical of projections of large economic benefits from stadium-districts, which supposedly defy the abundance of historical evidence [to the contrary].”

The new USL soccer team, Rhode Island FC, is scheduled to debut March 16. It plans to play its 2024 home games 10 miles away at Bryant University before the stadium in Pawtucket opens in 2025.