Munis were steady to weaker in spots Wednesday, while U.S. Treasuries were firmer after the Fed hiked rates 25 basis points and signaled more may come this year. Equities ended the session in the red.

The Fed just “delivered a 25bps hike and by holding firm to their data dependent rhetoric and are trying to keep the September meeting live with the possibility that this won’t be their final hike,” said Gordon Shannon, a partner and portfolio manager at TwentyFour Asset Management, a fixed-income boutique of Vontobel.

“The Fed is weighing arguments that lagged impacts from previous hikes are still being transmitted into the economy while watching carefully for signs of credit tightening by banks,” he said.

While Wednesday’s rate hike matters, Phillip Neuhart, director of market and economic research at First Citizens Wealth, said its impact is “far surpassed by the prior 5% worth of Fed hikes since March of 2022.”

“Tighter monetary policy takes time to feed into the economy, and thus, we are still feeling the impact of past hikes,” he said. “The U.S. economy remains resilient, but tighter monetary policy has slowed economic growth and could continue to do so.”

The two-year muni-to-Treasury ratio Wednesday was at 59%, the three-year at 60%, the five-year at 61%, the 10-year at 65% and the 30-year at 89%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 59%, the three-year at 60%, the five-year at 59%, the 10-year at 64% and the 30-year at 88% at 4 p.m.

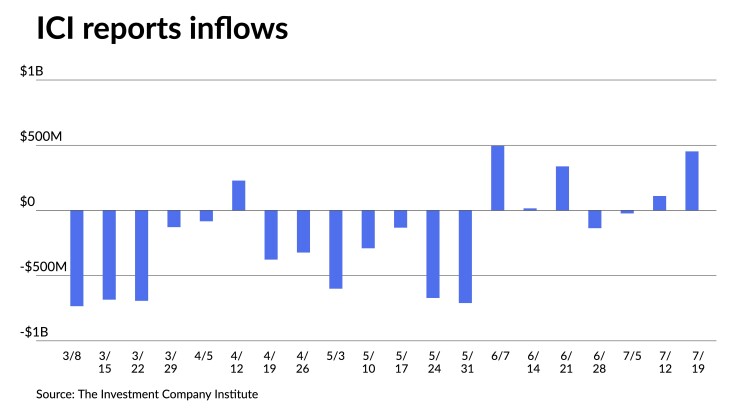

The Investment Company Institute reported investors added $453 million to municipal bond mutual funds in the week ending July 19, after $111 million of inflows the previous week. Exchange-traded funds saw inflows of $1.125 billion after $96 million of inflows the week prior.

Deal placement “has been respectable for a data-heavy week while secondary market metrics indicate month-end considerations are in play,” said Kim Olsan, senior vice president of municipal bond trading at FHN Financial.

Daily tallies are “accelerating into the close of the month,” she said.

Bloomberg reports that July’s figures are averaging $920 million, but she notes “the last week has brought an increase of 15% as sellers look to align portfolios and raise cash for syndicate settlements.”

Any daily amount over $1 billion par usually “signals a more volatile market, as this month’s totals closely mirror last July (both impacted to an extent with FOMC actions),” she said.

However, daily averages in July 2020 and July 2021 were below $500 million “as the market’s trading range was far narrower,” she said.

“One input to bids wanteds volume is how active the primary market is expected to be — and the current 30-day visible supply projection under $7 billion signals potentially less selling needs,” Olsan said.

The front half of the curve is “showing signs of normalization,” she said.

While the 5s1s MMD slope is still inverted at 50 basis points, she said “it’s down from negative 68 basis points in mid-May.”

Meanwhile, she said the 10s5s curve is essentially flat “after reaching an inversion of 11 basis points in early June.”

Those moves are “relevant to short-optioned structures that have created a prolonged conundrum for bidding to call dates rather than benched off maturity dates in premium 5s,” according to Olsan.

Past 10 years on the curve, she said the “sweet spot remains with about 70 basis points implied pickup out to 20-year maturities — not as steep as the 80 basis point slope wide but still well positioned for longer inquiry allocations.”

Absolute yields in the 15-year range “exceed 3.25% for TEYs approaching 5.50% and competitive with equity returns in recent years.”

Recent new-issue pricings point to opportunities in specific credits.

Washington’s large state GO sale on Tuesday saw levels in line with recent history.

The 10-year Washington GO “yielded 2.63%, or 13 basis points over the implied 10-year MMD spot,” she said, while a smaller sale of Hillsborough County, Florida, GOs came at the same yield and spread. “However, as evidence of exaggerated yields in Texas PSF-backed schools credits” a pricing of Royse City Independent School District, Texas, “netted a 10-year spread 35 basis points above the MMD spot,” Olsan said.

In the 20-year range, she said “the Washington and Hillsborough yields aligned with each other, spread +30/MMD.”

Meanwhile, the Royse City ISD yield was spread 13 basis points wider.

Credit spreads in the AA-rated space “show greater compression as strained supply conditions force tighter bidding,” she said.

Intermountain Power Agency, Utah, 5s due 2043 (Aa3/NR) “traded +25/MMD, or nearby trading in Texas PSF School GO 5% bonds,” she said.

In the primary market Wednesday, RBC Capital Markets priced for the North Carolina Housing Finance Agency (Aa1/AA+//) $199 million of non-AMT social homeownership revenue bonds, Series 51, with 3.25s of 7/2024 at par, 3.375s of 1/2028 at par, 3.4s of 7/2028 at par, 3.875s of 1/2033 at par, 3.9s of 7/2033 at par, 4.1s of 7/2038 at par, 4.375s of 7/2043 at par, 4.5s of 1/2048 at par and 5.57s of 1/2054 at 3.92%, callable 7/1/2032.

Q3 outlook

With a U.S. debt default avoided in the second quarter of the year, “investors can once again pivot back to assessing the relative value proposition among various fixed income sectors,” said Principal Asset Management strategists in a report.

They believe munis “offer a compelling opportunity for tax-sensitive investors as we move into the second half of 2023.”

Relative to USTs, munis offer “some of the most attractive entry points in several months,” they said.

The favorable technical backdrop that “frames the asset class gives us confidence that municipals will reverse recent cheapening and outperform over the next several months,” they noted.

More than $106 billion of the third quarter’s cash flow will come back to investors, which includes “all bonds maturing over July to September along with previously announced bond calls as well as interest payments,” they said. This is the highest of any quarter in 2023, Principal Asset Management strategists said.

At $140 billion, they said new-issue debt is “trailing 2022’s level by about 27% through the first six months of 2023.

July, August, and September are “historically among the lowest months of the year in terms of supply, further providing a tailwind to municipal levels,” they noted.

Secondary trading

Maryland 5s of 2024 at 3.05%-3.04% versus 3.04% Monday. Wisconsin 5s of 2025 at 2.92%. DC 5s of 2026 at 2.84%.

Washington 5s of 2028 at 2.62% versus 2.61% Tuesday. NYC 5s of 2028 at 2.70% versus 2.69% Tuesday. City and County of Denver 5s of 2029 at 2.54%-2.51%.

NYC 5s of 2032 at 2.67%-2.65% versus 2.73%-2.74% on 7/18. California 5s of 2033 at 2.42%. Indiana Finance Authority 5s of 2034 at 2.87% versus 2.88% Friday and 3.01% original on 7/19.

Baltimore County, Maryland, 5s of 2049 at 3.60%-3.61% versus 3.58% Monday. Massachusetts 5s of 2053 at 3.81%-3.80% versus 3.79%-3.80% Tuesday and 3.78%-3.75% Friday. Fort Lauderdale, Florida, 5s of 2053 at 3.85% versus 3.86% Monday and 3.85% original on 7/20.

AAA scales

Refinitiv MMD’s scale was cut three basis points out long: The one-year was at 3.02% (unch) and 2.85% (unch) in two years. The five-year was at 2.52% (unch), the 10-year at 2.50% (unch) and the 30-year at 3.49% (+3) at 3 p.m.

The ICE AAA yield curve was little changed: 3.02% (unch) in 2024 and 2.90% (unch) in 2025. The five-year was at 2.50% (unch), the 10-year was at 2.47% (-1) and the 30-year was at 3.47% (unch) at 4 p.m.

The S&P Global Market Intelligence (formerly IHS Markit) municipal curve was cut two basis points out long: 3.02% (unch) in 2024 and 2.85% (unch) in 2025. The five-year was at 2.52% (unch), the 10-year was at 2.51% (unch) and the 30-year yield was at 3.49% (+2), according to a 3 p.m. read.

Bloomberg BVAL was cut up to one basis point out long: 2.94% (unch) in 2024 and 2.83% (unch) in 2025. The five-year at 2.50% (unch), the 10-year at 2.45% (unch) and the 30-year at 3.46% (+1) at 4 p.m.

Treasuries were firmer.

The two-year UST was yielding 4.829% (-5), the three-year was at 4.470% (-6), the five-year at 4.099% (-7), the 10-year at 3.860% (-4), the 20-year at 4.128% (-2) and the 30-year Treasury was yielding 3.931% (-1) near the close.

FOMC

A unanimous Federal Open Market Committee decision raised interest rates 25 basis points, as expected, to a range between 5.25% and 5.5%, and left the door open for further rate hikes.

“In determining the extent of additional policy firming that may be appropriate to return inflation to 2% over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments,” the post-meeting statement said.

In his press conference, Fed Chair Jerome Powell spoke of a tight labor market and still too-high inflation, stressing effort to get inflation down to 2% “still has a long way to go.”

Responding to a question, Powell said the Fed would assess rates on a meeting-by-meeting basis, based on data, with the goal being bringing inflation down to 2%. “It is certainly possible” that rates will increase again in September, but it’s also “possible” for a Fed skip.

The Fed can be “patient” as well as “resolute,” he said, and that slowing doesn’t necessarily mean the Fed wouldn’t raise rates in two consecutive meetings, if needed. The Fed isn’t likely to cut rates this year, he added, but he refused to answer whether the Fed would cut rates if inflation was above 2%.

“This further cements the aggressive nature of the hiking cycle, and they may not be done,” said Olu Sonola, head of U.S. Economics at Fitch Ratings. “While recent inflation prints have been softer than expected, this is a Fed that does not want to declare mission accomplished. Inflation prints over the next two months are consequential to the future direction of the policy rate.”

The statement “maintained a hawkish bias,” said Thomas Holzheu, Swiss Re Chief Economist for the Americas. Although ”the meeting most likely represents the peak in the Fed’s historically rapid hiking cycle, upside risks to the policy rate persist as core inflation pressures remain well above target and economic conditions remain robust.”

The FOMC didn’t moderate “their characterization of growth, inflation, or employment, and they did not change the guidance they indicated in their June communication,” noted Ali Hassan, portfolio manager at Thornburg Investment Management.

While the market expects further inflation moderation should the Fed hike again this year, he said, “there is more and more chatter — pundits, academics and dovish Fed members — that the Fed should tolerate and will tolerate higher-for-longer inflation to preserve jobs and growth. After all, as inflation drops, real rates will be tightening.”

Gurpreet Gill, global fixed income macro strategist at Goldman Sachs Asset Management, noted the meeting “was one of the most certain and uncertain of the cycle.” The hike was expected, but the future is unclear, he said.

“We think recent data is consistent with the U.S. policy rate peaking in July, as core CPI inflation slowed sharply in June,” Gill said. “But any renewed signs of inflation strength in key data like the Employment Cost Index released on Friday and upcoming PCE inflation releases still have potential to extend the hiking path.”

“The Fed was careful to make nearly no change in the statement beyond hiking rates,” according to Morgan Stanley. “Core readings on inflation have softened recently but the Fed did not acknowledge this in the statement.”

“Tighter for longer is still the Fed’s default position,” said Morning Consult Chief Economist John Leer. “The relatively hawkish rhetoric in Chair Powell’s press conference today should be taken at face value: real short-term interest rates are still more likely to rise than they are to fall through the end of the year. While financial markets were ready to declare victory against inflation following the June CPI print, the Fed almost entirely discounted that one data point.”

But, Edward Moya, senior market analyst at OANDA, said, “The Fed is probably done and that is keeping soft landing hopes alive. … The Fed is keeping optionality for future rate increases but it probably won’t need them.”

The Fed’s tightening campaign is starting to impact the U.S. economy “and unless the housing market continues to heat up, the disinflation process should help bring rates back to target,” he said.

Lisa Pendergast, executive director at the Commercial Real Estate Finance Council, said the Fed’s tightening cycle, and their impact on interest rates “has cast a shadow on commercial and multifamily mortgage refinance opportunities and pushed commercial real estate valuations lower.”

Exacerbating the issue is the volume of low-interest CRE loans maturing through 2027 when office valuations have fallen.

“The combination of today’s higher mortgage rates and lower property valuations have and will continue to present significant challenges for owners of commercial real estate seeking to refinance maturing loans,” she said.

Primary to come:

The Medina Valley Independent School District, Texas (/AAA//), is set to price Thursday $363.690 million of PSF-insured unlimited tax school building bonds, Series 2023, serials 2026-2053. Raymond James & Associates.

The Charleston Educational Excellence Financing Corp., South Carolina (Aa3/AA-//), is set to price Thursday on behalf of the Charleston County School District $142.535 million of installment purchase revenue refunding bonds, Series 2023, serials 2023-2026, 2028. Wells Fargo Bank.

The Denison Independent School District, Texas (Aaa/AAA//), is set to price Thursday $131.405 million of PSF-insured unlimited tax school building and refunding bonds, Series 2023, serials 2024-2050. Raymond James & Associates.

The Minnesota Housing Finance Agency (Aa1/AA+//) is set to price Thursday $130 million of taxable social residential housing finance bonds, Series 2023J, serials 2023-2033, terms 2038, 2043, 2047, 2053. RBC Capital Markets.