The muni bond market grew in the second quarter as ownership by household and exchange-traded funds grew, while U.S. banks and insurers continued to reduce their holdings, the latest Federal Reserve data shows.

The face amount of munis outstanding ticked up to $4.129 trillion, a 1.1% increase from the first quarter of this year and a 1.8% increase from the second quarter of 2023, according to the latest Fed data.

The market value of munis was at $4.034 trillion, up 0.8% from the first quarter and up 2% from Q2 2023.

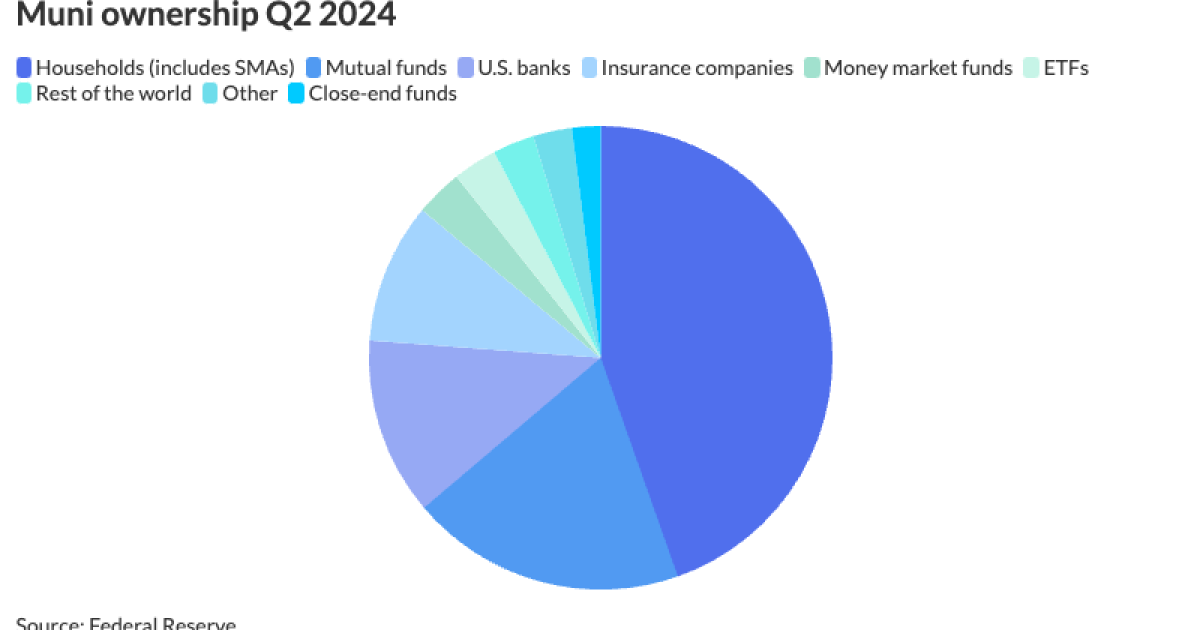

Household ownership of individual bonds was the largest category of muni ownership at 44.6%, mutual funds at 19.2%, ETFs at 3.1% and U.S. banks at 12.4%. Life insurance companies own 4.6% and property and casualty insurers at 5.2%.

The muni market has always been retail-driven, but now “we’re really a retail-driven market,” said Matt Fabian, a partner at Municipal Market Analytics.

“Demand is coming from individuals … either directly through an SMA or through a mutual fund, and has been more than sufficient

However, it’s not as “reliable” in the longer term, as a more diverse demand component would be better, which makes the market a bit more resilient to what is to come, Fabian said.

Once the Fed starts cutting rates, it will likely lead to a different yield curve, potentially changing individuals’ demand for munis, particularly if yields fall low enough to deter them, he said.

“So if the shape of the yield curve changes, it’s a question about how individual demand may change,” he said.

Household ownership of munis — which includes direct ownership of individual bonds in brokerage accounts, fee-based advisory accounts and separately managed accounts — rose to $1.798 trillion, up 2.4% from Q1 2024 and 6.9% in Q2 2023.

The surge of SMAs greatly contributed to the growth of household ownership, market participants said.

Although the Fed does not carve out SMA ownership, Bloomberg Intelligence and others on the Street peg it at as much as $1.6 trillion of munis.

“The market has structural demand for income and equality, so it’s no surprise that SMAs are rising,” said James Pruskowski, chief investment officer at 16Rock Asset Management

The asset management world is creating simpler solutions and better workstreams, as well as

SMA growth also stems in part from overall demand for tax-exempt paper, Howard said, noting this goes back to the 2017 Tax Cuts and Jobs Act, which included capping the state and local tax deductions, or SALT, said Cooper Howard, a fixed income strategist at Charles Schwab.

“For investors in states like California or New York, that caused a big deduction and resulted in their tax rates moving higher, causing them to seek out tax-exempt options,” he said, as munis are one of the few available.

That has contributed to SMA growth given the importance of California and New York in the muni market, which has trickled into other parts, Howard said.

Additionally, household net worth has increased to record level highs, pushing a number of individuals who might not have been municipal bond buyers to now become muni buyers, he said.

Like SMAs, ETFs have mostly seen increases in ownership.

ETFs rose 1.7% from the first quarter of this year and 15.7% year-over-year to $124.4 billion.

“A material change has occurred in the muni ETF space, as the value held at the end of June totaled $124 billion, up an impressive 93% since 2020,” said Kim Olsan, senior fixed income portfolio manager at NewSquare Capital. ”The ETF balance in 2020 represented a 7% share of muni mutual funds, but has since grown to [nearly] 16% share.”

The ETF market has attracted a lot of retail investors as they are very familiar with how ETFs trade, Howard said.

“It’s a simplistic way to get exposure to the muni market,” he noted.

Anecdotally, money has been moving out of mutual funds into SMAs and ETFs, contributing to ETF growth outpacing mutual fund growth.

Fed data shows mutual funds slightly increased their muni holdings quarter-over-quarter and year-over-year. Mutual funds owned $775.1 billion in Q2 2024, rising 0.5% from Q1 2024 and 1.5% from Q2 2023.

Part of the slight increase by mutual funds is “them not selling anymore, some inflows, and probably a larger part is market value gains,” Fabian said.

However, mutual funds are still down 13% since the end of 2020, Olsan noted.

Mutual funds are “still an important aspect of the market, but they’re starting to lose some of the importance because of the increase in SMAs and ETFs,” Howard said.

The main factor in the growth of ETFs is fees, said Roberto Roffo, a 30-plus year muni veteran.

“As investors have become more conscious of fees, they have been drawn to the lower fee structure of ETFs, which on average are 50% lower than mutual funds,” he noted.

Additionally, ETF growth has been more significant than mutual funds as the “liquidity of ETFs and being able to trade them all day long versus waiting until a mutual fund strikes its NAV at the end of the day is a big draw,” Roffo said.

The fee structure is important when it comes to total return over a longer period of time, he said.

“Most mutual funds manage to an index similar to ETFs and typically outperform or underperform by a slim margin,” Roffo said.

“The additional fee structure of mutual funds robs from the performance over the long term and makes it much more difficult to outperform a given index which has zero fees, he said.

The lower fees associated with ETFs make it “easier to compete versus its index over time because the fees are not subtracting as much from the performance,” according to Roffo.

Meanwhile, banks continue to shed their muni holdings.

Banks held were at $498.5 billion, down 3.3% quarter-over-quarter and 9.1% from Q2 2023. This is the lowest value since mid-2020, Olsan said.

“As banks were active buyers of long, low coupons in the 2020/2021 period, creation of long 2% coupons ceased in 2022 with rate hikes and subsequent trading ground to a halt on large losses,” she said. “Current yields have rallied in recent months to where vintage 2% production has shown material price recovery, potentially opening up the spigot for additional roll off of similar structures in a declining rate environment.”

“The reduction in ownership by banks is some selling, but also mostly banks are not reinvesting and steering their money into other asset classes,” Fabian said.

In the past, changes in bank behavior have reflected actions at just a few of the biggest banks, which would have an outsized impact on those numbers, he noted.

However, the pullback in Q2 was felt by nearly all of the top 20 banks cutting their muni holdings, according to Fabian.

Bank holdings of munis, though, may have stabilized in the third quarter, he said, citing fata from the Federal Reserve Bank of St. Louis.

“Munis aren’t getting any richer or any cheaper, so it could be that [banks] haven’t had their positions run off as quickly, or maybe banks are concerned that the corporate tax rate is going to rise, so it makes sense for them to not lose all their muni holdings,” Fabian said.

Munis need banks, and banks like munis because the asset class is safe, long and connected to “building things,” which are all things that banks like about an instrument, he said.

“So, banks don’t necessarily want to get rid of their munis, but sometimes they do,” Fabian said.