August saw an increase in supply for the eighth consecutive month as pent-up demand and front-loaded issuance led issuers to tap the capital markets, leading to the highest monthly total volume for August on record.

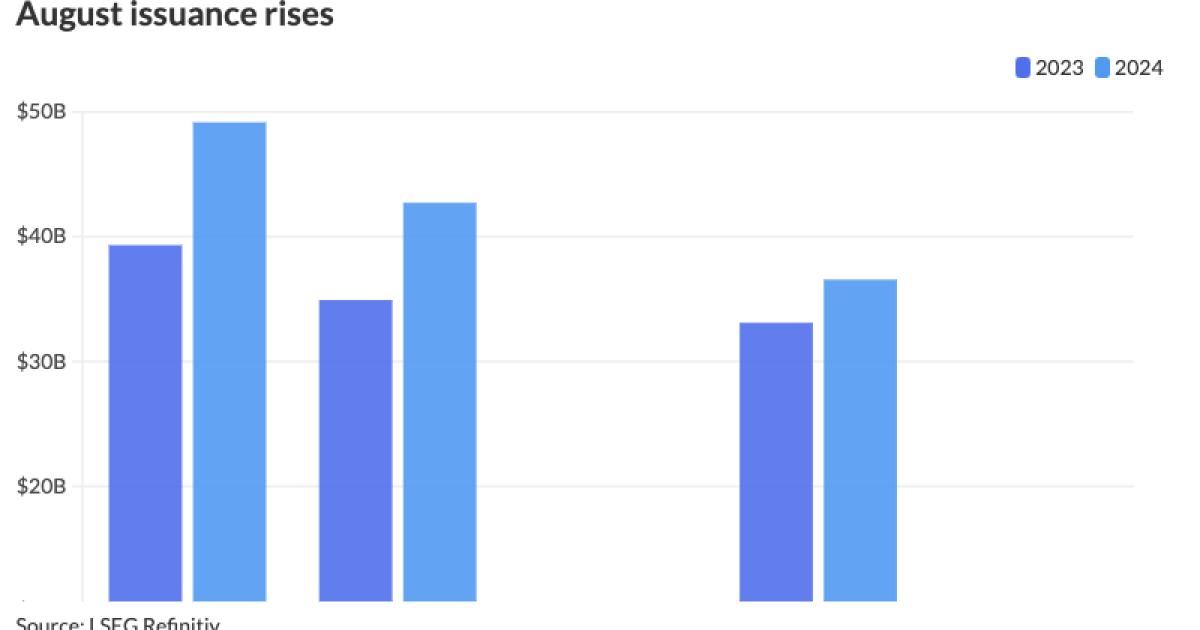

August’s volume reached $49.174 billion in 873 issues, up 25% from $39.33 billion in 827 issues in 2023. August’s total is above the 10-year average of $40.828 billion and is the highest monthly total this year.

Issuance year-to-date is at $334.621 billion, up 33.6% year-over-year.

“August’s supply was reflective of a more constructive forward rate path as issuers were incentivized to come to market while investors found reasons to be invested,” said Kim Olsan, senior fixed income portfolio manager at NewSquare Capital.

The market saw deals of “shapes and sizes” in August, said Steve McLaughlin, co-head of the municipal capital markets group at S&P Global Market Intelligence.

Some of the deals coming to market were “backlogged,” and there has been a demand for infrastructure funding, he said.

Additionally, “there’s so much pent-up demand to raise money for projects,” McLaughlin said.

And with COVID money having been spent, interest rates are about to reverse, and Fed rate cuts are on the horizon, it’s a “good time to issue when you have those market dynamics in place,” he said.

Tax-exempt issuance in August was at $42.727 billion in 812 issues, a 22.3% increase from $34.926 billion in 752 issues a year ago.

New-money and refunding volumes both increased. The former rose 10.4% to $36.568 billion from $33.108 billion, while the latter increased 76.8% to $5.296 billion from $2.996 billion.

Some sectors have seen robust issuance this year, such as healthcare and

In August, healthcare issuance stood at $3.44 billion, up 160.5% year-over-year, while transportation was at $9.231 billion, up $17.4 from August 2023, buoyed by the slew of airport deals.

August boasted $1.3 billion of BayCare Health System revenue refunding bonds from the Hillsborough County Industrial Development Authority, North Carolina.

There were also a slew of airport deals, the largest being nearly

“A lot of the dialogue has been about COVID funds drying up, and so people need to come back to the market. But healthcare and airports were fighting through their operations and fighting to survive for so long,” Javes said. “This is a return back to capital planning and budgeting and what is their long-term strategic needs, and that’s allowed them to come back to the market in force.”

Many of deals have an AMT component, he said, as AMT issuance is up nearly 100% year-over-year. Alternative-minimum tax issuance rose to $3.582 billion, up 98.5% from $1.804 billion.

Spreads are being affected by that as they widen out on the AMT space, Javes said.

“There are not as many natural buyers of that product as there would be in a more conventional tax-exempt or taxable issuance in the market, and the pricing reflects that,” he said.

Issuance has been front-loaded this year ahead of the November election.

Many of the issuers remember eight years ago when the market had a “pretty poor reaction” following Donald Trump’s victory, and they want to avoid any of that happening this year, therefore pulling issuance forward ahead of Nov. 1, Javes said.

This means there will be robust in September and October before supply drops off in November and December, he noted.

“Issuance is expected to be advanced ahead of November if recent election cycles are any indication,” Olsan said.

This means there will be robust in September and October before supply drops off in November and December

From 2014 through 2023 (excluding 2016 and 2020), supply averaged $67.233 billion between September and October, according to LSEG.

During election years, September and October issuance totaled $86.452 billion in 2016 and $96.876 billion in 2020, according to LSEG.

“Generic yields were quite favorable to issuers for both new-money and refunding purposes in each of those years (although 2020 brought greater limitations on the vehicles conducive to refunding),” she said.

Therefore, issuance in September and October 2024 should exceed 2023’s total of $70.19 billion.

More August issuance details

Revenue bond issuance increased 24.9% to $29.809 billion from $23.876 billion in August 2023, and general obligation bond sales rose 25.3% to $19.365 billion from $15.454 billion in 2023.

Negotiated deal volume was up 27% to $40.677 billion from $32.019 billion a year prior. Competitive sales increased 29.9% to $8.281 billion from $6.374 billion in 2023.

Bond insurance rose 44.1% to $3.785 billion from $2.626 billion.

Bank-qualified issuance fell 9.6% to $839.3 million in 215 deals from $928.2 million in 239 deals a year prior.

In the states, the Golden State claimed the top spot year-to-date.

Issuers in California accounted for $50.105 billion, up 41.5% year-over-year. Texas was second with $48.997 billion, up 4.1%. New York was third with $37.813 billion, up 50.6%, followed by Florida in fourth with $18.895 billion, up 123.3%, and Massachusetts in fifth with $10.614 billion, a 114.6% increase from 2023.

Rounding out the top 10: Washington with $9.681 billion, up 49.6%; Illinois with $9.236 billion, up 5.7%; Alabama with $7.981 billion, up 35.9%; Wisconsin with $7.725 billion, up 27.7%; and Virginia with $7.255 billion, up 77%.