Municipals felt the pressure of a U.S. Treasury market selloff, but outperformed their taxable counterparts, after better economic data sent investors flocking to equities in a risk-on trade.

Triple-A yields rose two to four basis points, depending on the yield curve, while UST saw losses of up to 15 basis points on the short end, moving municipal to UST ratios lower there.

Muni to UST ratios were lower after the day’s moves, with the two-year muni-to-Treasury ratio at 64%, the three-year at 66%, the five-year at 67%, the 10-year at 69% and the 30-year at 86%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 66%, the three-year at 68%, the five-year at 68%, the 10-year at 70% and the 30-year at 85% at 4 p.m.

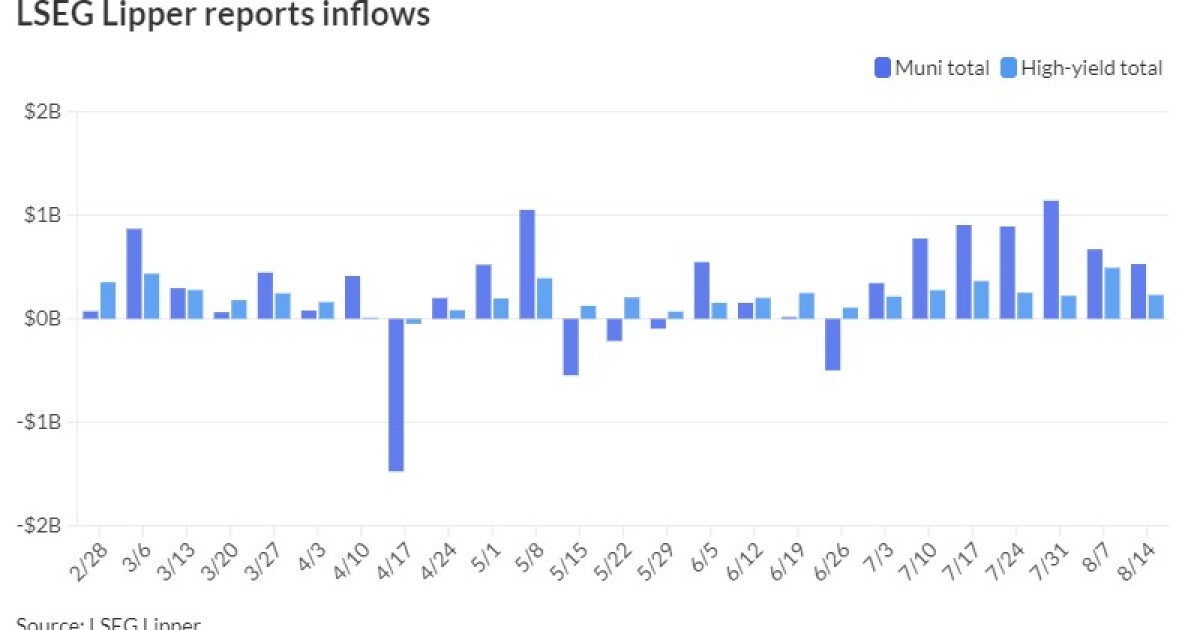

Municipal bond mutual funds saw inflows as investors added $528.7 million to funds after $674.1 million of inflows the week prior, according to LSEG Lipper. This marks seven straight weeks of inflows.

In the primary market Thursday, the final large deals of the week priced and were upsized in some cases.

Ramirez & Co. priced for institutions for the Triborough Bridge and Tunnel Authority (Aa3/AA-/AA+/AA+/) a slightly upsized $699.405 million of MTA Bridges and Tunnels Revenue Bonds deal, consisting of $308.55 million general revenue bonds, Subseries 2024 A-1, with 5s of 11/2035 at 3.03%, 5s of 2039 at 3.28%, 5s of 2044 at 3.65%, 5.25s of 2051 at 3.86% and 4s of 2054 at 4.20% (noncall), callable 11/15/2034; and $390.85 million general revenue refunding bonds, Subseries 2024 A-2, with 5s of 11/2025 at 2.69% (-2 from the preliminary scale), 5s of 2029 at 2.64% (-4), 5s of 2034 at 2.95%, 5s of 2039 at 3.28% and 5s of 2044 at 3.65%, callable 11/15/2034.

J.P. Morgan Securities LLP priced for the New Jersey Health Care Facilities Financing Authority (A2//AA-/) $251.570 million of Inspira Health Obligated Group Issues revenue and refunding bonds, Series 2024A, with 5s of 7/2025 at 2.59%, 5s of 2029 at 2.86%, 5s of 2034 at 3.15%, 5s of 2039 at 3.43%, 5.25s of 2049 at 4.05%, .4125s of 2054 at 4.31% (noncall), and 5.25s of 2054 at 4.14%, callable 7/1/2034.

BofA Securities priced for the Reno-Tahoe Airport Authority (A3/A//A+/) $240.88 million of airport revenue bonds, consisting of $161.9 million AMT-bonds, Series 2024A, with 5s of 7/2025 at 3.53%, 5s of 2029 at 3.60%, 5s of 2034 at 3.84%, 5.25s of 2039 at 4.02%, 5.25s of 2044 at 4.30%, 5.25s of 2049 at 4.35%, and 5.25s of 2054 at 4.44%; and $78.98 million non-AMT bonds, Series 2024B, with 5s of 2027 at 2.93%, 5s of 2029 at 2.90%, 5s of 2034 at 3.18%, 5s of 2039 at 3.51%, 5s of 2044 at 3.93%, 5s of 2049 at 4.06% and 5.25s of 2054 at 4.10%.

Bond Buyer 30-day visible supply grows to $17.64 billion just as investors began to digest about $15 to $20 billion of reinvestment cash hitting the market Thursday.

“This will boost demand in the 1-10 year portion of the market, in particular, with that sector of the market seeing particularly limited support thus far this week,” noted J.P. Morgan strategists.

“Raw yields are nominally lower from the end of July but the impetus to push to the next leg down will be dependent on how much of the redemption credits are reinvested,” said Kim Olsan, senior fixed-income portfolio manager at NewSquare Capital.

The reinvestment dollars being credited Thursday, which Olsan noted are slightly less than half the month’s total, comes in ahead of September’s $21 billion.

The historically lower reinvestment totals in September shows that since 2019, the month’s rate moves “have all been upwardly bound from August’s closing levels,” she said.

Short yields have “become more aligned with the 10-year range over the last month, resulting in a nominal 10 basis point gap between 1- and 5-year bonds — well flatter than the negative 70 basis points from the end of Q1,” Olsan noted.

She said a positively leaning slope from 5- to 10-year maturities “appears to be drawing in larger flows.”

However, the longer curve slope is “still an incentive for extension given the rate outlook in the coming six to 12 months,” she said.

Olsan noted the upcoming new-issue calendar offers long-dated maturities across names such as New York City GOs, which are trading around +25/AAA, and Dallas-Fort Worth airport with two large term bonds.

J.P. Morgan strategists see continued opportunities to buy bonds in the fall, “given the prospect of weaker election-related municipal market technicals.”

AAA scales

Refinitiv MMD’s scale was cut two to three basis points: The one-year was at 2.67% (+2) and 2.61% (+2) in two years. The five-year was at 2.56% (+2), the 10-year at 2.71% (+3) and the 30-year at 3.59% (+3) at 3 p.m.

The ICE AAA yield curve was better: 2.65% (-3) in 2025 and 2.61% (-3) in 2026. The five-year was at 2.53% (-3), the 10-year was at 2.67% (-2) and the 30-year was at 3.53% (-1) at 4 p.m.

The S&P Global Market Intelligence municipal curve was cut: The one-year was at 2.70% (+3) in 2025 and 2.68% (+3) in 2026. The five-year was at 2.58% (+3), the 10-year was at 2.70% (+3) and the 30-year yield was at 3.56% (+3) at 4 p.m.

Bloomberg BVAL was cut two to three basis points: 2.67% (+2) in 2025 and 2.64% (+2) in 2026. The five-year at 2.58% (+2), the 10-year at 2.65% (+3) and the 30-year at 3.57% (+3) at 4 p.m.

Treasuries sold off.

The two-year UST was yielding 4.097% (+15), the three-year was at 3.998% (+1), the five-year at 3.675% (-1), the 10-year at 3.831% (-2), the 20-year at 4.212% (-4) and the 30-year at 4.121% (-5) at the close.