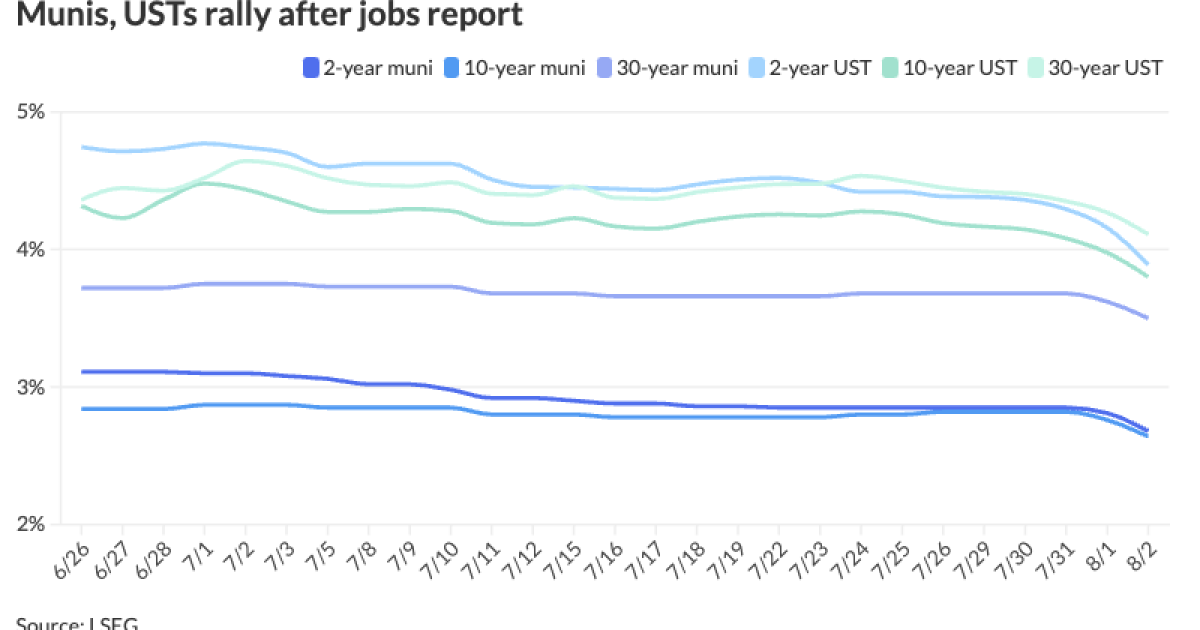

Municipals extended their rally Friday, underperforming U.S. Treasuries which saw yields plummet up to nearly 30 basis points on the short end after a weaker-than-expected nonfarm payrolls report. Equities sold off.

Muni yields were bumped nine to 14 basis points, depending on the scale, while UST yields fell 17 to 29 basis points, pushing two-, three-, five- and 10-year USTs to their 2024 lows.

The two-year muni-to-Treasury ratio Friday was at 69%, the three-year at 71%, the five-year at 71%, the 10-year at 69% and the 30-year at 85%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 64%, the three-year at 65%, the five-year at 66%, the 10-year at 66% and the 30-year at 82% at 3:30 p.m.

The bond market is rallying Friday on a weaker-than-expected jobs report and a bump in the unemployment rate, said Jeff Lipton, a research analyst and market strategist.

“The bond market clearly welcomed that news,” he said.

All eyes now turn to the September Federal Open Market Committee meeting where the Fed is expected to cut rates, but market participants are mixed on whether it will be a 25- or 50-basis-point cut.

“With this week’s dramatic shift in Fed sentiment and data suggestive of a path to even lower rates, munis substantially underperformed, which is not uncommon in seismic shifts in UST rates, paving the way for outperformance when volatility in the UST market subsides,” said J.P. Morgan strategists led by Peter DeGroot.

“The tax-exempt market remains rather vulnerable — if not for the massive rate rally, it would have now been in a much tougher position,” said Barclays strategists Mikhail Foux and Clare Pickering.

However, they said, lower yields and greater clarity surrounding Fed rate cuts this fall should have a “stabilizing effect.”

Issuance for the week of Aug. 5 surges to $13.733 billion — $10.752 billion of negotiated deals and $2.981 billion of competitive deals.

It will be one of the heaviest weeks in the past year, above the average $10 billion weekly issuance for non-holiday weeks over the past three months, J.P. Morgan strategists said.

The negotiated calendar is led by the Louisiana Public Facilities Authority with

Minnesota leads the competitive calendar with $1.6 billion of GOs in six series.

“The rest of August is also expected to be busy, while market activity and liquidity will likely continue declining, especially in the last two weeks of the month,” Barclays strategists said.

They are “somewhat skeptical” munis will continue to rally, and MMD-UST ratios may keep “drifting higher” in the near future.

“Current cheaper market valuations, coupled with the sizable $27 billion in early August coupon/redemption reinvestment capital, just $1 billion lower than the first half of July, should result in higher municipal bond valuation and outperformance, given stability in the UST market,” J.P. Morgan strategists said.

AAA scales

Refinitiv MMD’s scale was bumped 10 to 13 basis points: The one-year was at 2.70% (-13) and 2.68% (-13) in two years. The five-year was at 2.59% (-10), the 10-year at 2.64% (-12) and the 30-year at 3.50% (-12) at 3 p.m.

The ICE AAA yield curve was bumped 10 to 14 basis points: 2.71% (-14) in 2025 and 2.67% (-13) in 2026. The five-year was at 2.4% (-14), the 10-year was at 2.61% (-13) and the 30-year was at 3.50% (-10) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was bumped nine to 13 basis points: The one-year was at 2.74% (-11) in 2025 and 2.71% (-9) in 2026. The five-year was at 2.58% (-13), the 10-year was at 2.63% (-10) and the 30-year yield was at 3.47% (-11) at 3 p.m.

Bloomberg BVAL was bumped 11 to 12 basis points: 2.69% (-12) in 2025 and 2.66% (-12) in 2026. The five-year at 2.56% (-11), the 10-year at 2.58% (-11) and the 30-year at 3.48% (-11) at 3:30 p.m.

Treasuries rallied.

The two-year UST was yielding 3.876% (-29), the three-year was at 3.700% (-27), the five-year at 3.614% (-24), the 10-year at 3.789% (-19), the 20-year at 4.177% (-17) and the 30-year at 4.103% (-17) at 3:45 p.m.

Employment report

With nonfarm employment growing by just 114,000 jobs and the unemployment rate climbing to 4.3%, economists are looking for more from the Federal Reserve, although some note that it is just one report and may have been skewed by Hurricane Beryl.

“The Fed should have buyer’s remorse about its decision to leave rates unchanged on Wednesday,” said Chris Low, chief economist at FHN Financial. “Payroll growth kicked off Q3 weaker than any month in Q2, every month of which was, in turn, weaker than any single month in Q1.”

The unemployment rate is above what the Fed considers full employment, he noted. “Job growth was weak and has been weakening for months, with half the growth in the lowest-paying industries. The unemployment rate at 4.3% is now 0.9 percentage points above its 3.4% low, triggering the Sahm Rule,” Low said.

The Sahm Rule — often useful in identifying the start of a recession — “has now largely been met,” said Scott Anderson, chief U.S. economist and managing director at BMO Economics. “If the three-month average of the unemployment rate rises by 0.5 percentage points or more relative to its low during the previous 12 months a recession has begun.”

The unemployment rate rose nine-tenths of a percentage point since the January 2023 low of 3.4%, he noted.

The report’s weakness has the market pricing in a 60% likelihood of 50-basis-point cuts in both September and November, Low noted.

“Hurricane Beryl may have accounted for some of the weakness, but we are skeptical as there is no obvious evidence as payroll changes in construction, mining, and leisure and hospitality — areas usually sensitive to big weather events — were pretty close to typical,” Low said.

While “this is just one report,” he added, “the pace of labor market cooling has accelerated since March.”

Anderson agreed that data shows “that aggregate demand is softening rapidly. This clearly gives the Fed the green light to start cutting rates in September, and the market’s attention will now shift focus toward how many and how deep the coming cuts will be.”

“Markets are rightly reacting by significantly increasing the expected number of rate cuts in the near future,” said Manhattan Institute scholar Dan Katz, who called it “a categorically weak report.”

“Stepping back, this employment report is one that indicates modest weakness, not an impeding recession,” he said, meaning the Fed will not overact.

“Additionally, employment reports tend to be quite noisy and are subject to significant revisions,” Katz said, noting jobs are still being created, but at a slower pace.

“The dominant narrative in markets will become whether the Fed is ‘behind the curve,’ but only the economic data in coming months will reveal whether the U.S. economy has downshifted to a modestly slower growth paradigm, or whether a more severe downturn is beginning,” he said.

“This was a disappointing but not fatal jobs report,” said Josh Jamner, investment strategy analyst at ClearBridge Investments. “Across-the-board misses and softer data are consistent with slowing economic momentum signaled by [Thursday’s] ISM report, but we believe this is best characterized as normalization instead of the start of something worse.”

While much of the increase in the unemployment rate was from entrants to the workforce, he said, “on balance job creation remains in positive territory.”

Still, fewer hours worked and a decline in wages when added to low job creation, create “worries that the Fed is behind the curve in maintaining maximum employment,” Jammer said.

While he noted markets are leaning toward a 50-basis-point rate cut in September, “that outcome remains less likely than a 25 bp initial cut given that much of the data can be characterized as welcome normalization with the economy still firmly in net positive job creation territory.”

ING chief international economist James Knightley said he still expects three 25bp cuts this year, “but the risks do increasingly appear to be skewed to more aggressive action, especially in early 2025.”

While the Fed still has an eye on inflation, he said, “this week’s employment cost index and unit labor cost data should have boosted their confidence that inflation is on the path to 2%.”

“This was a ‘bad news is bad news’ report for the market and will continue the growth scare that has been roiling equities lately,” said Lara Castleton, U.S. head of portfolio construction and strategy at Janus Henderson Investors.

Fears of recession and a more aggressive Fed reaction are dominant, she noted. “While worries of a policy mistake are rising, one negative miss shouldn’t lead to overreaction,” she said. “GDP is still strong, average hourly earnings are rising and inflation is coming down.”

“Financial markets have turned their attention from ‘when and how much will the Fed ease’ to a ‘growth looks like it is plunging and the Fed is behind the curve’ mentality,” said Wells Fargo Investment Institute senior global market strategist Scott Wren. “Expect the near-term volatility to continue.”

The firm is pricing in two cuts this year and one next, he said. “The consensus and the Fed, in our view, are too optimistic on the magnitude of 2025 cuts.”

Seema Shah, chief global strategist at Principal Asset Management, wonders if the Fed made a policy mistake. She expects a September rate cut “and the Fed will be hoping that they haven’t, once again, been too slow to act.”

While the report was “softer than expected,” Giuseppe Sette, president of Toggle AI, said it “will do absolutely nothing to change the Fed’s course; payrolls can be volatile, and this is just one data point.”

“The Fed will need to go into economic protection mode moving forward to calm markets,” said Byron Anderson, head of fixed income at Laffer Tengler Investments. “We should see rate cuts shortly and the bond market is asymmetrically positioned lower for the short term.”

“The question isn’t will they cut in September, but by how much?” said Jay Woods, chief global strategist at Freedom Capital Markets. “With the Sahm rule officially being triggered, both the talk of recession and criticism of the Fed will grow louder.”

He said the market believes “the data-dependent Fed [was] too late to act again.”

“This week’s data does not suggest a rush for the Fed to cut rates aggressively,” said Subadra Rajappa, Societe Generale head of U.S. rates strategy. “The market pricing of cuts is also at odds with the continued easing of financial conditions.”

Primary to come

The Louisiana Public Facilities Authority (Baa3///) is set to price Tuesday $1.321 billion of AMT I-10 Calcasieu River Bridge P3 senior lien revenue bonds, Series 2024, terms 2054, 2059, 2064, 2066. J.P. Morgan.

The Long Island Power Authority (A2/A/A+/) is set to price Tuesday $1.021 billion of electric system general revenue bonds, consisting of $736.120 million of Series 2024A, serials 2025-2044, terms 2049, 2054, and $285.11 million of fixed-rate mandatory tender bonds, Series 2024B, terms 2049. BofA Securities.

The Florida Development Finance Corp. is set to price $985 million of non-rated Brightline Florida Passenger Rail Expansion revenue bonds, Series 2024A, Morgan Stanley.

The Trustees of California State University (Aa2/AA-//) are set to price Wednesday $682.3 million of systemwide revenue bonds, consisting of $670.645 million of tax-exempts, Series 2024A, serials 2025-2046, terms 2049, 2055, and $11.655 million of taxables, Series 2024B, serials 2025-2034, terms 2039, 2043. BofA Securities.

Chicago (/BBB+/A-/A) is set to price Wednesday $643.11 million of GOs, Series 2024A, serials 2041-2045. Huntington Securities.

The Hillsborough County Aviation Authority (Aa3//AA-/AA/) is set to price Thursday $483.875 million of AMT Tampa International Airport revenue bonds, 2024 Series B, serials 2027-2044, terms 2049, 2054. J.P. Morgan.

The University of Colorado Hospital Authority (Aa2/AA/AA/) is set to price Tuesday $389.99 million of revenue and revenue refunding bonds, consisting of $113.365 million of Series 2024A, serials 2029; $152.7 million of Series 2024B, serials 2025-2029, 2031, 2035-2039; and $132.925 million of Series 2024C, serials 2034. Jefferies.

The California Statewide Communities Development Authority (/A+/A/) is set to price Tuesday $389.565 million of fixed-mode John Muir Health revenue bonds, Series 2024A, serials 2025-2044, term 2049, 2054. BofA Securities.

Colorado Springs, Colorado, (Aa2/AA+//) is set to price Wednesday $385.2 million of utilities system revenue bonds, consisting of $294.865 million of improvement bonds, Series 2024A, serials 2030-2044, terms 2049, 2054; and $90.335 million of refunding bonds, Series 2024B, serials 2024-2028, 2030-2044. BofA Securities.

Atlanta (Aa3//AA-/AA+/) is set to price Tuesday $379.95 million of airport general revenue bonds, consisting of $235.95 million of non-AMT green bonds, Series 2024A-1, serials 2025-2044, terms 2049, 2054; $23.765 million of non-AMT bonds, Series 2024A-2, serials 2025-2034; and $120.235 million of AMT bonds, Series 2024B, serials 2034-2044, terms 2049, 2054. Siebert Williams Shank.

The Lower Colorado River Authority (/A/A+/) is set to price Tuesday $361.305 million of LCRA Transmission Services Corporation Project refunding revenue bonds, Series 2024A, serials 2026-2044, terms 2049, 2054. J.P. Morgan.

The Los Angeles Department of Water and Power (Aa2/AA-//AA) is set to price Thursday $355.3 million of power system revenue bonds, 2024 Series D, serials 2029-2032, 2036, 2038, 2041, 2043, 2045, 2047, 2050, 2052, 2054. Barclays.

The Chattanooga Health, Educational and Housing Facility Board (/A/A-/) is set to price Thursday $322.565 million of Erlanger Health health system revenue bonds, Series 2024. Morgan Stanley.

The Crowley Independent School District, Texas, (Aaa//AAA/) is set to price Wednesday $242.36 million of PSF-insured unlimited tax school building bonds, Series 2024, serials 2025, 2027-2054. Siebert Williams Shank.

The Los Angeles County Facilities Inc. (/AA+/AA+/) is set to price Wednesday $220.745 million of Vermont Corridor Site 2 lease revenue bonds, consisting of $215.23 million of tax-exempts, Series 2024A, serials 2029-2045, term 2049, 2054, 2057, and $5.545 million of taxables, Series 2024B, serials 2028-2029. Barclays.

Alaska (Aa3/AA//AA/) is set to price Tuesday $193.49 million of GO refunding bonds, consisting of $96.85 million of Series 2024B, serials 2026-2035, and $96.64 million of forward-delivery bonds, Series 2025A, serials 2026-2035. Jefferies.

The National Finance Authority, New Hampshire, is set to price Thursday $176.66 million of Tamarron Project special revenue bonds, Series 2024, serial 2035. Wells Fargo.

The Nebraska Investment Finance Authority (/AAA//) is set to price Wednesday $174.085 million of social non-AMT single-family housing revenue bonds 2024 Series E, serials 2025, 2030-2036, terms 2039, 2044, 2049, 2049, 2054. J.P. Morgan.

Cook County, Illinois, (/AA-/AA/AAA) is set to price Tuesday $168.165 of sales tax revenue refunding bonds, Series 2024, serials 2024-2044. Loop Capital Markets.

The Okaloosa School Board, Florida, (Aa3/AA/AA/) is set to price Tuesday $159.95 million of Assured Guaranty-insured certificates of participation, Series 2024, serials 2025-2044, terms 2049. BofA Securities.

The Colorado Housing and Finance Authority (Aaa/AAA//) is set to price Wednesday $150.355 million of taxable single-family mortgage bonds, Class I, 2024 Series E-1, serials 2026-2036, terms 2039, 2043, 2049. RBC Capital Markets.

The South Carolina State Housing Finance and Development Authority (Aaa///) is set to price Tuesday $150 million of non-AMT mortgage revenue bonds, Series 2024 B, serials 2025-2036, terms 2039, 2044, 2049, 2054, 2055. BofA Securities.

The Pecos-Barstow-Toyah Independent School District, Texas, (/AAA//) is set to price Thursday $144.28 million of PSF-insured unlimited tax school building bonds, Series 2024, serials 2025-2043. Frost Bank.

The New Braunfels Independent School District, Texas, is set to price Thursday $125 million of unlimited tax school building bonds, Series 2024. Piper Sandler.

The Iowa Finance Authority (Aaa/AAA//) is set to price Tuesday $123.32 million of single-family mortgage bonds, consisting of $64.3 million of non-AMT social bonds, 2024 Series E, serials 2035-2036, terms 2039, 2044, 2044, 2049, 2049, 2054, and $59.02 million of taxables, 2024 Series F, serials 2025-2034, terms 2039, 2044, 2049, 2054. RBC Capital Markets.

The Massachusetts Development Finance Agency (Aa1/AA+/) is set to price Thursday $108 million of Williams College issue revenue bonds, Series 2024V. Goldman Sachs.

The Development Authority of Burke County, Georgia, (Baa1/A/A-/) is set to price Wednesday $100 million of Georgia Power Company Plant Vogtle Project pollution control revenue bonds, Second Series 2012. Goldman Sachs.

Competitive

The Louisville and Jefferson County Metropolitan Sewer District, Kentucky, (Aa3/AA//) is set to sell $105.61 million of sewer and drainage system revenue bonds, Series 2024A, at 10 a.m. Eastern Tuesday.

Minnesota (Aaa/AAA/AAA/) is set to sell $449.25 million of GO state various purpose bonds, Series 2024A, Bidding Group 1, at 10:45 a.m. Eastern Tuesday; $444.725 million of GO state various purpose bonds, Series 2024A, Bidding Group 2, at 11:15 a.m. Tuesday; $352.75 million of GO state trunk highway bonds, Series 2024B, at 10:15 a.m. Tuesday; $30.965 million of taxable GO state various purpose bonds, Series 2024C, at 12:45 p.m. Tuesday; $192.715 million of GO state various purpose refunding bonds, Series 2024D, at 11:45 a.m. Tuesday; and $141.225 million of GO state truck highway refunding bonds, Series 2024E, at 12:15 p.m. Tuesday.

Oyster Bay, New York, is set to sell $185.24 million of bond anticipation notes, at 10:30 a.m. Eastern Thursday.

Gary Siegel and Layla Kennington contributed to this report.