After selling off last week, municipals saw some pressure ease as triple-A yields rose only a few basis points while U.S. Treasuries were weaker and equities ended mixed.

Municipal to UST ratios were steady. The two-year muni-Treasury ratio Monday was at 71%, the three-year at 72%, the five-year at 71%, the 10-year at 69% and the 30-year at 89%, according to Refinitiv MMD’s 3 p.m. ET read. ICE Data Services had the two-year at 73%, the three-year at 74%, the five-year at 71%, the 10-year at 71% and the 30-year at 92% at 4 p.m.

The muni market “was not immune to the Treasury selloff, succumbing to the pressure as the week wore on,” said Birch Creek strategists in a weekly report.

“Muni bonds slid … as the fixed income markets sold off as the Fed hinted that the Federal Reserve may continue to raise interest rates,” said Jason Wong, vice president of municipals at AmeriVet Securities.

This caused the “yields in the front end of the muni curve to jump by 27 basis points to hit the highest since mid-March,” he said.

Since the 52-week low on April 12, he said “yields have risen by an average of 46 basis points.”

With yields rising last week, munis “underperformed versus Treasuries as 10-year notes are now yielding 68.78% of Treasuries compared to the week prior when the ratios were at 68.29%” according to Wong.

The benchmark AAA curve “underperformed by 2-6bps out to 10 year, while keeping pace with Treasuries out to 30 year,” Birch Creek strategists said.

The front end of the curve, they noted, “was hit the hardest due to the surge in supply coming from the FDIC portfolio of failed bank holdings.”

Their sales last week were “focused on maturities inside of 10 years, which spurred a large uptick in customer purchases in this part of the curve,” they said.

Out longer, Birch Creek strategists said “activity was in line with recent trends as most accounts looked to the primary market to add paper.

The jump in rates “has pushed the month of May into negative return territory as prior to this sell off, munis were up 0.40% for the month but today were at now down to 0.46%,” he said.

The front end of the curve “has underperformed in the broader markets as it has only returned 0.67%, while long bonds have returned 3.43% year to date,” according to Wong.

This volatility in the markets, he noted, “has put pressure on the primary markets and has forced some issuers to postpone their deals.

Trading for last week “totaled to roughly $42.89 billion for the week with 55% of the trades being dealer sells and with majority of the trading being the front end,” he said.

With the sharp rise in yields in the front end, Wong said “it comes to no surprise that the front end had a lot of activity last week.”

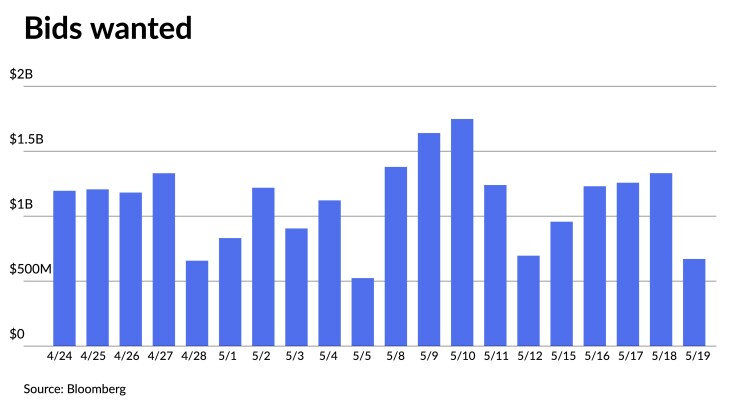

Clients put up around $5.4 billion up for the bid, down from $6.7 billion the prior week, according to Bloomberg data.

Investors pulled around $187 million from muni bond funds, marking the 14 straight weeks of outflows, which Birch Creek strategists said continues to be manageable.

“While interest rates look a lot more reasonable at current levels, the muni market will need to get through the rest of the [FDIC failed bank muni] list before it can perform again,” they said.

Around “70% of the list is left, with mostly longer-duration bonds,” they noted.

While the low-coupon structure is usually “not a fit for most accounts,” Birch Creek strategists said there will be a “knock-on effect as accounts have to absorb $5 billion of extra paper.”

“Now that rates have backed up and spreads on lower coupon structures are wider,” they believe this is a “good time to get invested before the strong summer technical kicks in.”

In the competitive market Monday, the Madison Metropolitan School District, Wisconsin, (/AA+//) sold $105 million of GO debt to BofA Securities, with 5s of 3/2024 at 3.45%, 5s of 2028 at 2.79%, 5s of 2033 at 2.80%, 4s of 2038 at 3.96% and 4.125s of 2043 at 4.17%, callable 3/1/2030.

Secondary trading

NYC 5s of 2024 at 3.34% versus 3.05% Wednesday and 3.00% on 5/11. Washington 5s of 2024 at 3.35% versus 3.35% Friday and 3.00% on 5/11. Massachusetts 5s of 2024 at 3.20%-3.19%.

Maryland 5s of 2026 at 2.98%-2.95%. Triborough Bridge and Tunnel Authority 5s of 2027 at 2.90%-2.86%. Massachusetts Clean Water Trust 5s of 2028 at 2.69%-2.70%.

NYC Municipal Water Finance Authority 5s of 2031 at 2.57%. Virginia College Building Authority 5s of 2033 at 2.92% versus 2.75% Thursday and 2.70% original on Wednesday. Metropolitan County, Minnesota, 5s of 2035 at 2.85%-2.83% versus 2.60% original on Wednesday.

Crosby ISD, Texas, 4s of 2046 at 4.22%-4.11%. Illinois Finance Authority 5s of 2051 at 4.44% versus 4.16% on 5/16 and 4.20% on 5/10.

AAA scales

Refinitiv MMD’s scale was cut up to two basis points: The one-year was at 3.26% (unch) and 3.05% (unch) in two years. The five-year was at 2.67% (+2), the 10-year at 2.57% (+2) and the 30-year at 3.52% (unch) at 3 p.m.

The ICE AAA yield curve was cut three to eight basis points: 3.35% (+3) in 2024 and 3.11% (+4) in 2025. The five-year was at 2.71% (+3), the 10-year was at 2.60% (+3) and the 30-year was at 3.62% (+8) at 4 p.m.

The IHS Markit municipal curve was cut up to two basis points: 3.25% (unch) in 2024 and 3.05% (unch) in 2025. The five-year was at 2.67% (+2), the 10-year was at 2.56% (+2) and the 30-year yield was at 3.52% (unch), according to a 4 p.m. read.

Bloomberg BVAL was cut one to three basis points: 3.10% (+2) in 2024 and 2.98% (+1) in 2025. The five-year at 2.63% (+2), the 10-year at 2.55% (+3) and the 30-year at 3.58% (+2) at 4 p.m.

Treasuries were weaker.

The two-year UST was yielding 4.324% (+6), the three-year was at 3.991% (+4), the five-year at 3.770% (+4), the 10-year at 3.721% (+5), the 20-year at 4.101% (+4) and the 30-year Treasury was yielding 3.970% (+4) at 4 p.m.

Primary to come:

The New Jersey Transportation Trust Fund Authority (A2/A-/A/A/) will price $674 million of Series AA transportation program bonds on Thursday. Jefferies.

The authority (A2/A-/A/) is also set to price $262.780 million of Series A transportation system bonds on Thursday. Jefferies.

San Antonio, Texas, (Aa2/AA-/AA-/) is set to price $589.995 million of electric and gas systems revenue and revenue refunding bonds on Tuesday. Serials 2024 to 2044; term in 2050. Loop Capital Markets.

The Department of Water and Power of the city of Los Angeles (Aa2/AA+/AA/) is set to price $485.475 million of 2023 Series A water system revenue refunding bonds on Tuesday. Serials 2023 to 2044; terms 2049 and 2053. Wells Fargo Bank.

The Metropolitan Washington Airports Authority (Aa3/AA-/AA-/) is set to price $433.115 million of Series 2023 A airport system revenue and refunding bonds subject to the AMT on Wednesday. Barclays Capital.

The Pennsylvania Housing Finance Agency (Aa1/AA+//) is set to price $387.270 million of Series 2023 -142A, non-AMT single-family mortgage revenue social bonds on Wednesday. Serials 2028 to 2034; terms in 2038, 2041, 2043, 2046, 2048, 2050, 2053. Jefferies.

The Oregon Department of Transportation (Aa2/AA+/AA+/) is set to price $210.640 million of Series 2023 A highway user tax revenue subordinate lien bonds on Wednesday. Serials 2035 to 2042. Wells Fargo Bank.

The Fremont, California, Union High School District (Aaa/AAA//) is set to price $210 million of Series 2023 general obligation bonds on Tuesday. Morgan Stanley.

Pflugerville, Texas, (Aa1///AA+) is slated to price $153 million of combination tax and limited revenue certificates of obligation Series 2023 bonds on Tuesday. Serials 2024 to 2043; terms 2048 and 2053. Sibert Williams Shank.

Fort Bend County, Texas, (Aa1//AA+/) is set to price $134.090 million of Series 2023 A, B, and C bonds on Tuesday. J.P. Morgan Securities.

The Iowa Finance Authority (Aaa/AAA//) is set to price $130.750 million of 2023 Series C non-AMT and Series D taxable single-family mortgage-backed bonds on Tuesday. Morgan Stanley.

Georgetown, Texas, (/AA//) is set to price $101.400 million of Series 2023 utility system revenue bonds insured by Build America Mutual Assurance Co. on Wednesday. Serials 2024 to 2043; terms 2048, 2053. Bok Financial Securities.

San Antonio, Texas, (Aa3/A-plus/AA-minus/) is set to price $100.300 million of electric and gas systems variable rate junior-lien Series 2023 revenue refunding bonds on Wednesday. Term in 2053. Barclays Capital.

Brazoria County, Texas, Industrial Development Corp. is set to price $100 million of solid waste disposal facilities revenue bonds for the Aleon Renewable Metals LLC Project on Wednesday. Truist Securities.

Competitive:

Forsythe, North Carolina, (Aaa/AAA/AAA/) is set to sell $127.7 million of GO paper on Tuesday in two deals.