Municipals faced pressure on the short end, with the one- and two-year yields rising two basis points, while U.S. Treasuries saw gains on bonds inside five-years and equities were in the black.

For municipals, Monday’s session was more about readying for the primary and prepping for month-end positioning.

Municipal-to-UST ratios showed the 5-year at 53%, the 10-year at 74% and the 30-year at 83%, according to Refinitiv MMD. ICE Data Services had the 5-year at 53%, 10-year at 75% and the 30 at 84%.

A bearish sentiment still underlies the municipal bond market, with a notably soft bid-side, according to Jeff Lipton, managing director of municipal credit research at Oppenheimer Inc. Lipton said municipal market sentiment will be driven by movements in Treasury bond prices, and a dramatic sell-off in that market could catalyze a reversal in municipal bond mutual fund flows.

“Despite the back-up in yields and ratios, retail remains tentative,” Lipton said Monday, noting spreads have been widening in the new-issue market.

CreditSights noted that tax-exempts are reliant on direct or indirect buying from individual investors, “which may get a boost next week when issuers pay out $23 billion of principal and interest payments on Nov. 1.”

While fundamental metrics are in flux, “the one definitive move has been a higher yield set with more attractive taxable equivalent yields in play,” said Kim Olsan, senior vice president at FHN Financial. She noted the 5-year AAA spot closed out January at 0.22% (0.35% taxable equivalent yield in the 37% bracket), and now offers a TEY just shy of 1%. Intermediate TEYs have moved up from around 1.15% at the beginning of the year to near 2% and long high-grade TEYs sit at 2.75%, up more than 50 basis points over the course of the year.

“Past 10 years where coupon variability comes into play, the increase is even greater — 20-year 3s are trading at real yields that bump the TEY to near 3.25% vs. around 2.40% during Q1,” she said.

For now, munis are outperforming Treasuries, both on a month-to-date and year-to-date basis, Lipton said.

“We have reason to believe that the better relative returns can be sustained,” he said.

On the other side of this technical dynamic, supply trends are often driven by issuer sentiment, capital needs, views on interest rates, legislative developments, and revenue and budgetary conditions.

Thirty-day visible supply sits at $13.21 billion. But as the final weeks of the year approach, Lipton said, “there will continue to be ample cash awaiting deployment guidance and we do not see demand being fully satisfied even with ebbing bond redemptions and maturing securities over the near-term.”

Secondary trading

South Carolina 5s of 2022 at 0.10%. Mecklenburg County, North Carolina, 5s of 2022 at 0.10%. Texas 5s of 2023 at 0.28%. Tennessee 5s of 2023 at 0.29%.

Wake County, North Carolina, 5s of 2024 at 0.34%-0.33%. Oregon 5s of 2024 at 0.42%. California 5s of 2025 at 0.54%.

New York EFC 5s of 2029 at 1.07%. California 5s of 2030 at 1.25%. Georgia 5s of 2032 at 1.30% versus 1.26% on Oct. 19.

Monmouth County, New Jersey, 5s of 2034 at 1.43% versus 1.37% original. University of North Carolina Chapel Hill 5s of 2035 at 1.42%-1.37%.

Hennepin County 5s of 2037 at 1.49%-1.44%.

AAA scales

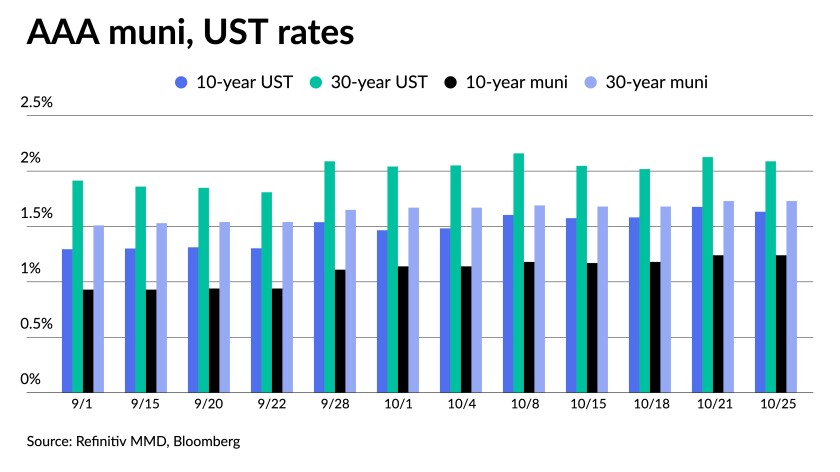

According to Refinitiv MMD, the short end saw yields rise two basis points to 0.15% in 2022 and 0.23% in 2023. The yield on the 10-year was steady at 1.24% and the yield on the 30-year stayed at 1.73%.

The ICE municipal yield curve showed bonds rise two basis points to 0.17% in 2022 and two to 0.24% in 2023. The 10-year maturity stayed at 1.20% and the 30-year yield sat at 1.75%.

The IHS Markit municipal analytics curve showed short yields steady at 0.15% in 2022 and 0.21% in 2023. The 10-year yield sat at 1.22% and the 30-year yield sat at 1.73%.

The Bloomberg BVAL curve showed short yields up one to 0.17% in 2022 and steady at 0.19% in 2023. The 10-year yield was up one at 1.23% and the 30-year up one to 1.76%.

In late trading, Treasuries were little changed as equities were up near the close.

The 5-year Treasury was yielding 1.175%, 10-year Treasury was yielding 1.633% and the 30-year Treasury was yielding 2.088%. The Dow Jones Industrial Average gained 57 points, or 0.16%, the S&P rose 0.48% while the Nasdaq gained 0.94%.

Economy

Since the Federal Reserve appears to be using the playbook from the last recovery, which is quite different from the current problems, one analyst said it is likely to end badly.

“There is a growing risk that the Fed is forced to make a major policy pivot sometime in the next two year,” according to Ethan Harris, global economist at BofA Securities.

This recovery results from supply issues, unlike the demand problems in the previous crisis, he said. The recovery in the labor market has been much quicker than the previous downturn, and “a strong consensus” exists suggests achieving full employment next year, five years earlier than the last time.

“This raises the question: is unusually dovish Fed policy needed to achieve this outcome or are they throwing gasoline on the fire?” Harris asked. And while “it’s too early for a definitive answer,” he said, “clearly the risks are rising.”

BofA is focusing on the job openings and labor participation rates, inflation expectations, median and trimmed inflation measures, and what happens with wage pressures when more workers return.

But, demand has risen in addition to the supply shortages, Berenberg chief economist for the U.S., Americas and Asia Mickey Levy said in a report. “While supply chain disruptions have been widely identified as the culprit, inflation has reflected a combination of supply shortages and strong demand. Aggregate demand has risen at a rapid pace.”

To prove the point, he cites nominal final sales to domestic purchasers, which fell 7.8% in the second quarter of last year, but jumped 17.2% in the next four quarters, “its fastest year-over-year pace in modern history, lifting it 7.2% above its pre-pandemic level.”

The price increases seen reflect more than just supply shortage, Levy said. The supply chain bottlenecks occurring now “cannot generate persistent inflation,” he asserted. “Persistent inflation occurs when aggregate demand persistently exceeds sustainable productive capacity, which historically has been driven by accommodative monetary policy.”

When supply issues abate, he said, prices that soared as a result, will decline. However, the price increases in “some, like shelter, are expected to accelerate,” Levy said.

And further monetary policy stimulus will lead to demand gains, he said. “If monetary and fiscal policies generate spending as they are designed, then excess demand will keep inflation elevated,” Levy said. “This suggests the risks of inflation are decidedly to the upside.”

In data released Monday, two regional Fed reports suggested growth slowed.

The Texas Manufacturing Outlook Survey reported slightly slower economic growth, while prices continued climbing and worker shortages remain.

“Costs are soaring higher with not much relief in sight,” said Emily Kerr, Dallas Fed senior business economist. “More than three-quarters of manufacturers say their raw materials prices increased further in October, and a majority expect prices to be even higher six months from now. Commentary from firms points to increased distress over shortages of materials and escalating costs. Manufacturers are also continuing to have trouble finding the workers they need, and the survey’s wage measures remain highly elevated. Despite these challenges, outlooks improved modestly.”

Separately, the Chicago Fed National Activity Index fell to negative 0.13 in September from positive 0.05 in August, suggesting below-average economic growth in the U.S. in the month.

The index’s three-month moving average, CFNAI-MA3, slid to 0.25 in September from 0.38 in August.

Primary market to come

Main Street Natural Gas (Aa2//AA-/) is on the day-to-day calendar with $750 million of gas supply revenue bonds, Series 2021A, serials 2023-2031, term 2052. RBC Capital Markets.

Dallas and Fort Worth, Texas, (A1//A+/AA/) is set to price Tuesday $708.1 million of Dallas Fort Worth International Airport joint revenue refunding bonds, taxable Series 2021C, serials 2022-2036, term 2046. Barclays Capital.

Dallas and Fort Worth, Texas, (A1//A+/AA) is also set to price Thursday $300.6 million of Dallas Fort Worth International Airport joint revenue refunding bonds, Series 2021B (non-AMT), serials 2022-2030 and 2043-2045. RBC Capital Markets.

California Community Choice Financing Authority (A2///) is set to price $556.03 million of clean energy project green revenue bonds, Series 2021A (climate bond certified). Goldman Sachs & Co.

AdventHealth Obligated Group (Aa2/AA/AA//) is set to price Wednesday $400 million of corporate CUSIP taxable hospital revenue bonds, Series 2021E. J.P. Morgan Securities.

Westchester County Local Development Corp. (non-rated) is set to price $392.245 million of revenue bonds (Purchase Senior Learning Community Inc. Project), Series 2021, consisting of $213.805 million of Series A, $23.52 million of Series B, $58.73 million of Series C, $89.525 million of Series D and $6.665 million of Series Ser E. HJ Sims & Co.

Ohio (Aa1/AA+/AA+//) is set to price Wednesday $326.055 million of general obligation bonds consisting of: $137.495 million of infrastructure improvement general obligation bonds, Series 2021A-II, serials 2022-2041; $40.355 million of conservation projects general obligation bonds, Series 2021A-CP, serials 2022-2034; $48.325 million of infrastructure improvement general obligation refunding bonds, Series 2021B, serials 2025-2032 and $99.88 million of common schools general obligation refunding bonds, Series 2021C, serials 2026-2032. Citigroup Global Markets.

Lancaster County Hospital Authority (A2/A+///) is set to price Wednesday $296.475 million of revenue bonds (Penn State Health), Series 2021. J.P. Morgan Securities.

The Health and Educational Facilities Board of the Metropolitan Government of Nashville and Davidson County, Tennessee, (A3/A///) is set to price Thursday $293.205 million of taxable revenue bonds (Vanderbilt University Medical Center), Series 2021A and 2021B. J.P. Morgan Securities.

The Industrial Development Authority of Phoenix, Arizona, (non-rated) is set to price Thursday $232.815 million of hotel revenue bonds (Provident Group — Falcon Properties LLC, Project), consisting of $143.585 million, Series A-1, terms 2041, 2051 and 2057; $7.785 million, Series A-2, term 2032 and $81.445 million, Series B, serial 2057. RBC Capital Markets.

Austin, Texas, (//AA-/) is set to price Wednesday $218.08 million of water and wastewater system revenue refunding bonds, Series 2021. Morgan Stanley & Co.

The Indiana Finance Authority (Aaa/AAA/AAA/) is set to price $215.03 million of state revolving fund program bonds, Series 2021B (green bonds). Citigroup Global Markets.

Wisconsin Health and Educational Facilities Authority (A1/AA-//) is set to price Tuesday $209.44 million of revenue bonds, Series 2021 (Aspirus, Inc. Obligated Group), serials 2034-2041, term 2051. Barclays Capital.

Private Colleges & University Authority (A2//AA-/) is set to price Wednesday $161.88 million of revenue bonds (The Savannah College of Art & Design Projects), Series 2021. Goldman Sachs & Co.

Miami-Dade County Health Facilities Authority (/A/A+/) is set to price Tuesday $157.38 million of hospital revenue and revenue refunding bonds (Nicklaus Children’s Hospital Project), Series 2021A, serials 2022-2042, terms 2046 and 2051. J.P. Morgan Securities.

Manor Independent School District is set to price Thursday $156.515 million of taxable unlimited tax refunding bonds, Series 2021B, serials 2022-2044. Jefferies LLC.

Bethel School District No. 403, Pierce County, Washington, (Aaa///) is set to price Tuesday $146.81 million of unlimited tax general obligation improvement and refunding bonds, 2021, insured by Washington State School District Credit Enhancement Program. Piper Sandler & Co.

California Statewide Communities Development Authority (/AA-/AA/) is set to price Wednesday $135.13 million of health facility revenue bonds (Montage Health), Series 2021A. Piper Sandler & Co.

Lamar Consolidated Independent School District, Fort Bend County, Texas, (Aaa/AAA//) is set to price Tuesday $134.57 million of unlimited tax refunding bonds, Series 2021A, serials 2023-2045, insured by the Permanent School Fund guarantee program. Wells Fargo Corporate & Investment Banking.

Successor Agency to the Redevelopment Agency of the City and County of San Francisco (/A//) is set to price $107.34 million of taxable third lien tax allocation bonds, 2021 Series A (affordable housing projects) (social bonds), serials 2023-2031. Citigroup Global Markets.

Clovis Unified School District (/AA-//) is set to price Thursday $100.815 million of federally taxable 2021 certificates of participation, serials 2022-2036, terms 2041, 2046 and 2051. Stifel, Nicolaus & Company.

Competitive:

Milwaukee County (//AA/) is set to sell $95.82 million of taxable general obligation pension promissory notes, Series 2021A, $10.53 million of general obligation transit promissory notes, Series 2021C; and $4.18 million of general obligation promissory notes, Series 2021B at 11:15 a.m. eastern Tuesday.

Los Angeles (//AA/) is set to sell $211.94 million of general obligation bonds, Series 2021-A (taxable) (social bonds) at noon Wednesday and $65.63 million of general obligation refunding bonds, Series 2021-B at 12:30 p.m. eastern Wednesday.

Montgomery County, Maryland, (/AA+//) is set to sell $57.465 million of taxable limited obligation certificates (Facility and Residential Development Projects) Series 2021A Taxable at 10:30 a.m. eastern, and $41.81 million of taxable limited obligation refunding certificates (Facility and Residential Development Projects) Series 2021B at 10:45 a.m. eastern Thursday.