Municipals were a touch weaker 10 years and in on thin trading while U.S. Treasuries pared back earlier losses the curve flattening continued.

Triple-A benchmarks saw one basis point cuts in spots inside 10-years while the five-year U.S. Treasury hit a high of 1.154% and the 30-year pared back earlier losses to land at 2.018%.

In the primary Monday, the North Texas Municipal Water District (Aa1/AAA//) sold $201.835 million of water system revenue refunding bonds to Morgan Stanley & Co. LLC. Bonds in 9/2022 with a 4% coupon yield 0.14%, 5s of 2026 at 0.58%, 4s of 2031 at 1.36% and 3s of 2032 at 1.55%, callable Sept. 1, 2030.

“The tone of the market is apprehensive due to interest rates trending higher, and fund flows weakening somewhat,” Michael Pietronico, chief executive officer at Miller Tabak Asset Management, said.

Pietronico noted his firm believes the one- to three-year area of the municipal yield curve will be the best performer in the coming weeks as supply moves higher and the Federal Reserve begins to taper its bond purchases.

“Overall, inflows have slowed down significantly, but are still positive, with high-yield seeing some outflows,” Roberto Roffo, managing director and portfolio manager at SWBC Investment Company, added.

“Most likely, investors are seeing their statements from last quarter and pulling back a little,” he said.

With ratios backing up significantly from historic lows and spreads widening slightly, there is a good opportunity for investors to restructure portfolios more advantageously, according to Roffo.

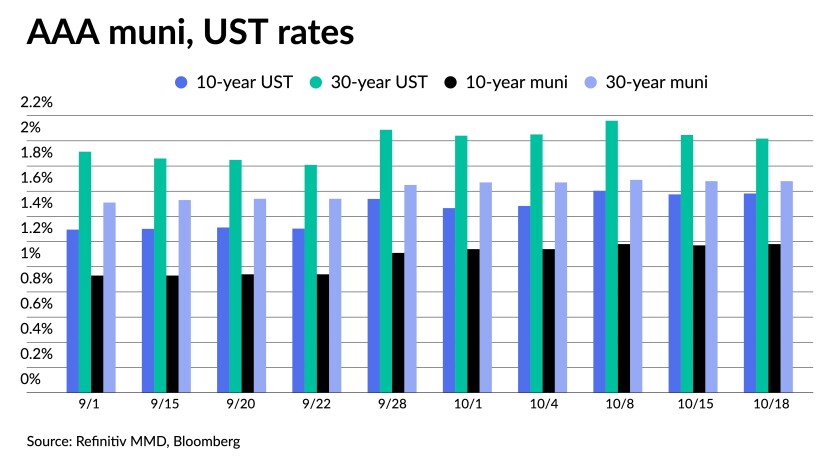

Ratios were held to near Friday’s levels, with the 10-year municipal-to-UST ratio at 74% and the 30-year at 83%, according to Refinitiv MMD. ICE Data Services had the 10-year at 73% and the 30 at 84%.

“Even with the decrease in inflows there is still significant cash on the sidelines to purchase new issues that present value,” he said. “This has been proven [last] week as large deals priced cheaper than they would have been a couple of months ago, were well subscribed for with little or any balances left over.”

Muni CUSIP requests fall

Monthly municipal volume decreased in September, the third consecutive monthly decline in muni CUSIP request volume following seven straight months of increases, according to CUSIP Global Services.

The aggregate total of all municipal securities, including municipal bonds, long-term and short-term notes, and commercial paper, fell 6.6% versus August totals. On an annualized basis, municipal CUSIP identifier request volumes were down 1.3% through September. For muni bonds specifically, there was a 9.9% decrease in request volumes month-over-month, but they are up 3.1 % on a year-over-year basis

“The three-month decline in municipal identifier request volume is definitely a trend to watch,” said Gerard Faulkner, direct of operations for CUSIP Global Services. “Municipal issuers were tapping the debt markets at a strong pace for much of 2020 and the first part of 2021, but that pace has now fallen off considerably.”

CUSIP identifier requests for the broad category of U.S. and Canadian corporate equity and debt climbed 3.3% versus August totals. The increase was driven largely by an increase in requests for domestic corporate debt identifiers. On a year-over-year basis, corporate CUSIP request volume rose 0.1%

Secondary trading

Nevada 5s of 2022 at 0.16%. West Virginia 5s of 2022 at 0.16%. Gilbert, Arizona, 4s of 2023 at 0.24%. Maryland 5s of 2023 at 0.20%.

Anne Arundel 5s of 2025 at 0.44%. New York Dorm PIT 5s of 2025 at 0.40%. Princeton 5s of 2025 at 0.37%. California 5s of 2025 at 0.47%.

New Castle, Delaware, 5s of 2027 at 0.76% versus 0.77% on 10/5. Wisconsin 5s of 2028 at 0.90%. New Mexico 5s of 2031 at 1.29%.

AAA scales

According to Refinitiv MMD, short yields were steady at 0.12% in 2022 and at 0.18% in 2023. The yield on the 10-year rose one basis point to 1.18% and the yield on the 30-year sat at 1.68%.

The ICE municipal yield curve showed bonds rise one basis point to 0.13% in 2022 and one to 0.18% in 2023. The 10-year maturity rose one to 1.14% and the 30-year yield was steady at 1.70%.

The IHS Markit municipal analytics curve showed short yields unchanged at 0.12% in 2022 and 0.18% in 2023. The 10-year yield sat at 1.15% and the 30-year yield was steady at 1.68%.

The Bloomberg BVAL curve showed short yields steady at 0.16% in 2022 and 0.17% in 2023. The 10-year yield rose one to 1.16% and the 30-year was steady at 1.70%.

In late trading, Treasuries were softer as equities were mixed.

The 10-year Treasury was yielding 1.582% and the 30-year Treasury was yielding 2.018% near the close. The Dow Jones Industrial Average lost 36 points, or 0.10%, the S&P rose 0.34% while the Nasdaq gained 0.84%.

Economy

Treasury yields should remain below average levels for quite some time, one analyst said.

“Given the obstacles the pandemic has produced, it is difficult to envision yields reaching even average levels in the near future,” said John Gentry, senior portfolio manager at Federated Hermes. “Consistent strong growth and growing inflation expectations would be required to push longer yields appreciably higher.

The 10-year Treasury yield has risen above 1.5% from its lows of 0.5% in July 2020. Wells Fargo Investment Institute Strategists Michelle Wan and Doug Beath suggest, “the current rising yield environment represents investor confidence in future economic growth and higher inflation expectations, sustaining a positive correlation between the 10-year Treasury yield and S&P 500 Index.”

But, Wan and Beath said, they don’t expect the rise “to be a straight line.” They see “consolidation and even pullbacks” resulting from political and economic events.

While investors have been keyed on growth expectations more than inflation concerns, “that could be changing,” they said. “Even so, over the longer term, we believe that bonds will continue to offer diversification benefits and should be held at allocations that are aligned with risk tolerance.”

In data released Monday, industrial production declined 1.3% in September after a downwardly revised 0.1% dip in August, while capacity utilization fell to 75.2% from 76.2%.

Economists polled by IFR Markets expected production to rise 0.2% and capacity use at 76.5%.

The decline reflects “production bottlenecks as manufacturers fall further behind healthy gains in product demand,” said Berenberg chief economist for the U.S., Americas and Asia Mickey Levy. The drop sets industrial production back below its pre-pandemic level, he said, underlining the various problems facing an array of manufacturing sectors.”

Motor vehicle and energy were two sectors showing big drops in production.

Part of the drop can be attributed to weather, said Wells Fargo Securities Senior Economist Tim Quinlan and Economist Shannon Seery. “While Hurricane Ida is partially to blame, accounting for nearly half of the decline, we cannot chalk up all of the weakness to its harsh effects,” they said. “Severe supply constraints are limiting the pace of production and are showing little sign of meaningful improvement.”

Supply issues persist with little indication of easing, they said. Additionally, high prices and labor shortages are impacting manufacturers.

“Supply chain disruptions will continue to deplete inventories,” said KC Mathews, chief investment officer at UMB Bank. “This may impact consumption; consumers that are willing and able to spend can’t if items are not on the shelf.”

And while this will remain an issue for GDP this year, he said, “the issue is clearly transitory. As bottlenecks are resolved and inventories restored, spending will resume in the near future.”

Also released Monday, the National Association of Home Builders’ Housing Market Index jumped to 80 in October from 76 in September. Economists expected the index to hold at 76.

“Builders are getting increasingly concerned about affordability hurdles ahead for most buyers,” NAHB Chief Economist Robert Dietz said. “Building material price increases and bottlenecks persist and interest rates are expected to rise in coming months as the Federal Reserve begins to taper its purchase of U.S. Treasuries and mortgage-backed debt.”

Separately, the New York services sector grew “modestly” in October, while prices continued to climb, and employment improved, according to the Federal Reserve Bank of New York’s Business Leaders Survey.

Respondents expect improvement in the next six months.

Primary to come

The Central Puget Sound Regional Transit Authority (Aa1/AAA///) is set to price Tuesday $874.83 million of sales tax and motor vehicle excise tax improvement and refunding green bonds, Series 2021S-1. J.P. Morgan Securities.

OhioHealth Corp. (Aa2/AA+/AA+/) is set to price Tuesday $600 million of taxable corporate CUSIP bonds, Series 2021. $300 million bullet due on 11/15/2031 and $300 million bullet due 11/15/2041. Barclays Capital Inc.

California Community Choice Financing Authority (A2///) is set to price $564.315 million of Climate Bond certified green clean energy project revenue bonds, Series 2021A, serials 2023-2027, term 2052. Goldman Sachs & Co.

The Hudson Yards Infrastructure Corp. (Aa2/AA-/A+//) is set to price Wednesday $451.985 million of Hudson Yards revenue green bonds, Fiscal 2022 Series A, serials 2026-2047. Goldman Sachs & Co.

Banner Health, Arizona, (/AA-/AA-//) is set to price Thursday $424.2 million of corporate CUSIP taxable bonds, Series 2021A. Morgan Stanley & Co.

Utah Transit Authority is set to price $361.355 million of taxable sales tax revenue refunding bonds, Series 2021 and federally taxable subordinated sales tax revenue refunding bonds, Series 2021, consisting of $344.985 million of Series 21 seniors (Aa2/AA/AA/) and $16.37 million, Series 21 subs (Aa3/AA-/AA/). Wells Fargo Corporate & Investment Banking.

University of Wisconsin Hospitals and Clinics Authority (Aa3/AA-///) is set to price Thursday $350.575 million of revenue bonds, Series 2021B green bonds and taxable revenue refunding bonds, Series 2021C. J.P. Morgan Securities.

Brockton, Massachusetts, (A1/AA-//) is set to price Tuesday $300 million of taxable pension obligation bonds, serials 2022-2035. Stifel, Nicolaus & Company.

The Wisconsin Public Finance Authority is set to price $263.63 million of revenue bonds (Searstone CCRC Project), consisting of: $104.85 million of Series 2021 A (non-rated), $36.31 million of Series 2021 B-1 (non-rated), $32.24 million of Series 2021 B-2 (Caa3////), $5.315 million of Series 2021 C (non-rated), $8.92 million of Series 2022 A (non-rated) and $75.995 million of Series 2023 A (non-rated). HJ Sims & Co.

Southwestern Community College District, San Diego County, California, (Aa2/AA-//) is set to price Wednesday $257.62 million, consisting of $73.62 million of Series 1, $3.05 million of Series 2 and $180.95 million of Series 3. Morgan Stanley & Co.

California Earthquake Authority (non-rated) is set to price Tuesday $250 million of revenue notes, Series 2021A. J.P. Morgan Securities.

Crown Point Multi-School Building Corp. (Lake County, Indiana) (/AA+//) is set to price Thursday $247.015 million of ad valorem property tax first mortgage bonds, Series 2021, insured by Indiana State Aid Intercept Program. Raymond James & Associates.

Dallas, Texas, (/A/A+/) is set to price Tuesday $236.595 million of hotel occupancy tax revenue refunding bonds, Series 2021, serials 2022-2038. Ramirez & Co.

The Virginia Housing Development Authority (Aa1/AA+//) is set to price Wednesday $226.63 million of taxable rental housing bonds, 2021 Series J, serials 2024-2036, terms 2041, 2046, 2051 and 2056. Raymond James & Associates, Inc.

The Indiana Finance Authority (Aaa/AAA/AAA//) is set to price $215.03 million of state revolving fund program green bonds, Series 2021B, serials 2023-2041. Citigroup Global Markets Inc.

The California Statewide Communities Development Authority (Baa1///) is set to price Tuesday $192.06 million of student housing revenue bonds (University of California, Irvine East Campus Apartments, Phase I Refunding & Phase IV-B CHF-Irvine, L.L.C.), Series 2021, serials 2023-2046, terms 2051 and 2054. Jefferies.

The Louisiana Public Facilities Authority (non-rated) is set to price Thursday $184.895 million, consisting of: $182.985 million of revenue and refunding revenue bonds, Series 2021A-1 (CommCare Corp. Project) and $1.91 million of taxable revenue bonds, Series 2021A-2 (CommCare Corp. Project). Piper Sandler & Co.

Carilion Clinic Obligated Group (Aa3/AA-//) is set to price Wednesday $180 million of taxable bonds, Series 2021. Goldman Sachs & Co.

The Wildwood Utility Dependent District, Florida, (/AA//) is set to price Tuesday $167.965 million of utility revenue bonds and subordinate utility revenue bonds, Series 2021 (South Sumter Utility Project), consisting of $146.56 million, Series 2021, serials 2025-2041, terms 2046 and 2051 and $21.405 million, Series 2021B, serials 2025-2041, terms 2046 and 2051. Jefferies.

The Triborough Bridge and Tunnel Authority (Aa3/AA-/AA-/AA) is set to price Thursday $163.245 million of MTA Bridges and Tunnels general revenue bonds, Series 2002F & Subseries 2008B-2 (conversion to fixed rate), consisting of $110.61 million, Series 2021 and $52.635 million, Series 2021B. Jefferies.

The Ohio Water Development Authority (Aaa/AAA//) is set to price Tuesday $150 million of water development revenue bonds, Fresh Water Series 2021. Goldman Sachs & Co.

The Ohio Housing Finance Agency (Aaa///) is set to price Tuesday $149.995 million of residential mortgage revenue bonds (Mortgage-Backed Securities Program), 2021 Series C (Non-AMT) (social bonds). J.P. Morgan Securities.

The Massachusetts Housing Finance Agency (/AA//) is set to price Thursday $149.105 million of housing bonds: consisting of $76.155 million, 2021 Series B-1 (sustainability bonds), serials 2024-2032, terms 2036, 2041, 2046, 2051, 2056, 2061 and 2063; $64.145 million, 2021 Series B-2 (sustainability bonds), serial 2023, terms 2025-2026; and $8.805 million, 2021 Series C, serial 2023. Barclays Capital.

American Municipal Power, Inc. (A1/A///) is set to price Wednesday $141.550 million of

Prairie State Energy Campus project revenue bonds, refunding series 2021A, serials 2032-2034 and 2036-2038. BofA Securities.

Bay Area Water Supply & Conservation Agency (Aa3/AA-//) is set to price Thursday $135.115 million of forward delivery refunding revenue bonds (Capital Cost Recovery Prepayment Program), Series 2023A. Goldman Sachs & Co.

The Wisconsin Public Finance Authority is set to price $133.02 million of non-rated hospital revenue bonds Celina Regional Medical Center, consisting of $106.22 million, Series A-1, terms 2031, 2041, 2051 and 2056 and $26.8 million, Series A-2, term 2040. KeyBanc Capital Markets.

Blue Springs, Missouri, Reorganized School District #4 of Jackson County (/AA+//) is set to price $132.79 million of general obligation school bonds, insured by Missouri Direct Deposit Program, consisting of: $107 million, Series A, serials 2030-2041 and $25.79 million, Series B, serials 2022-2025. Stifel, Nicolaus & Company.

The Successor Agency to the Redevelopment Agency of the City and County of San Francisco is set to price Thursday $130 million of 2021 Series A taxable third-lien tax allocation bonds affordable housing projects social bonds. Citigroup Global Markets Inc.

Clovis Unified School District, Fresno County, California, (/AA//) is set to price Thursday $122.725 million of 2021 taxable refunding general obligation bonds, Series B, serials 2022, 2026 and 2028-2039. Stifel, Nicolaus & Company.

The Georgia Housing and Finance Authority (/AAA//) is set to price Wednesday $101.235 million of single-family mortgage bonds, 2021 Series A (Non-AMT), serials 2022-2033, terms 2036, 2041, 2046 and 2051. Citigroup Global Markets.

Competitive

Fayetteville, North Carolina, (Aa2/AA/AA/) is set to sell $96.405 million of Public Works Commission revenue bonds, Series 2021 at 11 a.m. eastern Tuesday.

The Virginia Public School Authority (Aa1/AA+/AA+/) is set to sell $150.33 million of school financing bonds (1997 Resolution), Series 2021C at 10:30 a.m. eastern Tuesday.

Tusla, Oklahoma (Aa1/AA//) is set to sell $102.95 million of general obligation bonds, Series 2021 at 11:30 a.m. eastern Wednesday.