Municipals were a touch weaker as U.S. Treasuries and equities seesawed throughout the day on debt ceiling news out of Washington while new issues in the primary were in high demand and repriced to lower yields.

Triple-A benchmarks saw cuts of one to two basis points. Refinitiv MMD cut two on the 10-year and one on the 30-year while IHS Markit cut one on both maturities. Bloomberg BVAL cut its 10-year one basis point, leaving the 30-year unchanged while ICE Data Services bumped its one-year a basis point and left the rest of the curve little changed.

The 10-year municipal-to-UST ratio is at 76% and the 30-year at 81%, according to Refinitiv MMD. ICE Data Services had the 10-year at 75% and the 30 at 77%.

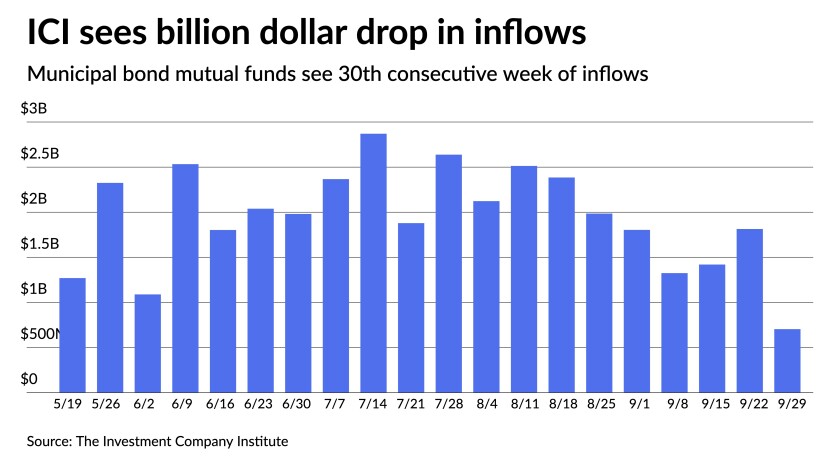

Another round of inflows was reported from the Investment Company Institute —the 30th consecutive week — but they were down $1.1 billion from a week prior. ICI reported $704 million of inflows for the week ending Sept. 29.

Exchange-traded funds saw $247 million of inflows after $233 million a week prior.

Total inflows have hit $76 billion year-to-date.

Participants will be watching for Refinitiv Lipper numbers Thursday as a gauge of how this week’s quieter open to the month affected investor sentiment.

CreditSights noted in a report earlier this week it is not concerned about a slowdown in flows into mutual funds, but rather a reversal of flows “because of the potential risks to secondary market prices if mutual funds are forced to sell long-duration bonds to raise cash to pay exiting shareholders.”

Tax-exempt municipal money market fund assets fell again, this time by $65.2 million from a week earlier.

In the primary, BofA Securities priced for the Alabama Federal Aid Highway Finance Authority (Aa2/AAA//) $1.49 billion of taxable special obligation revenue bonds. Bonds priced at par: in 9/2022 0.229%, 1.268% in 2026, 2.056% in 2031, and 2.65% in 2037, subject to a make whole call.

Siebert Williams Shank & Co. priced and repriced $317.34 million of general obligation green bonds with three to 10 basis point bumps for the School District of Philadelphia (A2//A+/). The first series, $267.375 million of Series A, saw 5s of 2022 at 0.18% (-10), 5s of 2026 at 0.76% (-4), 5s of 2031 at 1.58% (-4), 4s of 2041 at 2.22%, and 4s of 2046 at 2.37% (-3), callable Sept. 1, 2031. The second series, $49.965 million, saw 5s of 2022 at 0.18% (-10), 5s of 2026 at 0.76% (-4) and 5s of 2031 at 1.58% (-4), noncallable.

Barclays Capital Inc. priced for the State Public Works Board of the state of California (Aa3/A+/AA-/) $294.67 million of forward delivery lease revenue refunding bonds. Bonds in 8/2023 with a 5% coupon yield 0.68%, 5s of 2026 at 1.08%, 5s of 2031 at 1.82%, 5s of 2036 at 2.05%, 4s of 2037 at 2.25%, callable Aug. 1, 2031, dated Sept. 29, 2022.

RBC Capital Markets priced for Montgomery County, Ohio, (A1//AA-/) $240.65 million of hospital facilities revenue bonds (Dayton Children’s Hospital). Bonds in 8/2025 with a 5% coupon yield 0.46%, 5s of 2026 at 0.63%, 5s of 2031 at 1.43%, 4s of 2036 at 1.99%, 4s of 2041 at 2.20%, 4s of 2046 at 2.38%, 2.95s of 2051 at par and 4s of 2051 at 2.45%.

RBC Capital Markets priced and repriced for the Equitable School Revolving Fund $217.81 million of national charter school revolving loan fund social revenue bonds with up to nine basis point bumps, especially out long. The deal was three times oversubscribed. The deal consisted of $122.895 million of charter school revolving loan fund social revenue bonds for the Arizona Industrial Development Authority (/A//), with 4s of 2022 at 0.29%, 5s of 2026 at 0.89%, 4s of 2031 at 1.69%, 4s of 2036 at 2.05%, 4s of 2046 at 2.37% and 4s of 2051 at 2.42%, callable in 11/1/2031, and $25 million of subordinate series (nonrated), 4s of 2051 at 2.77%, callable in 11/1/2031.

Bonds issued for the California Infrastructure and Economic Development Bank, $31.555 million, saw 4s of 2032 at 1.70%, 4s of 2036 at 1.94%, 4s of 2041 at 2.11%, 4s of 2046 at 2.23%, 5s of 2051 at 2.28% and 4s of 2056 at 2.39%; $17.925 million for the Massachusetts Development Finance Agency, 4s of 2046 at 2.28% and 4s of 2051 at 2.34%; and, $25 million for Albany, New York Capital Resource Corp., 4s of 2046 at 2.30% and 4s of 2051 at 2.37%.

Rhode Island (Aa2/AA/AA/) sold $90.5 million of general obligation bonds to Mesirow Financial. Bonds in 8/2022 with at 5% coupon yield 0.15%, 5s of 2026 at 0.57%, 5s of 2031 at 1.28%, 2s of 2036 at 2.05% and 2.25s of 2041 at 2.30%, callable Aug. 1, 2031.

Rhode Island (Aa2/AA/AA) sold $44.5 million of taxable general obligation bonds consolidated capital development loan of 2021 to Wells Fargo Corporate & Investment Banking. Bonds in 8/2022 with a 3% coupon yield 0.20%, 1.12% at par in 2026, 1.84% coupon to yield 1.85% in 2031, at 2.45% par in 2036 and a 2.6% coupon to yield 2.65% in 2041, callable Aug. 1, 2031.

Richland County School District, South Carolina, (Aa/AA//) sold $74.995 million of unlimited tax general obligation bonds to JPMorgan Securities LLC. Bonds in 3/2022 with a 5% coupon yield 0.14%, 5s of 2026 at 0.50%, 4s of 2031 at 1.28%, 2s of 2036 at 1.95% and 2s of 2039 at 2.08%.

Informa: Money market muni funds fall again

Tax-exempt municipal money market fund assets fell by $219 million, lowering their total to $89.48 billion for the week ending Sept. 28, according to the Money Fund Report, a publication of Informa Financial Intelligence.

The average seven-day simple yield for the 150 tax-free and municipal money-market funds sat at 0.01%, the same as the previous week.

Taxable money-fund assets fell by $52.77 billion, bringing total net assets to $4.382 trillion. The average, seven-day simple yield for the 765 taxable reporting funds sat at 0.02%, same as the prior week.

Secondary trading

Short end trades showed strength. Massachusetts 5s of 2022 at 0.11%. North Carolina 5s of 2022 at 0.11%. Florida PECO 5s of 2023 at 0.20%.California 5s of 2023 at 0.21%. Maryland DOT 5s of 2024 at 0.30% and 5s of 2025 at 0.42%. Maryland 5s of 2025 at 0.39% versus 0.41% Tuesday.

New York City TFA 5s of 2026 at 0.61%. Ohio 5s of 2026 at 0.59%. Washington Suburban Sanitation District 5s of 2027 at 0.67%. Minnesota 5s of 2029 at 1.09%.

California 5s of 2029 at 1.06%. California 5s of 2030 at 1.17%. Massachusetts 5s of 2031 at 1.20%. Maryland 5s of 2032 at 1.23%.

Georgia 5s of 2033 at 1.24%. NYC TFA 5s of 2034 1.56%.

Texas waters 3s of 2040 at 1.92% versus 1.94% original. Washington 5s of 2042 at 1.70%.

AAA scales

According to Refinitiv MMD, short yields were steady at 0.13% and at 0.20% in 2022 and 2023. The yield on the 10-year rose two basis points at 1.16% while the yield on the 30-year rose one to 1.68%.

The ICE municipal yield curve showed bonds fall one in 2022 to 0.14% and steady at 0.19% in 2023. The 10-year maturity sat at 1.11% and the 30-year yield as steady at 1.70%.

The IHS Markit municipal analytics curve showed short yields steady at 0.14% and 0.19% in both 2022 and 2023. The 10-year yield was up one to 1.13% and the 30-year yield was up one to 1.67%.

The Bloomberg BVAL curve showed short yields steady at 0.16% and 0.16% in 2022 and 2023. The 10-year yield was up one to 1.13% and the 30-year yield was up one to 1.69%.

In late trading, Treasuries were softer as equities were up.

The 10-year Treasury was yielding 1.528% and the 30-year Treasury was yielding 2.082%. The Dow Jones Industrial Average gained 102 points, or 0.30%, the S&P rose 0.41% while the Nasdaq was up 0.47%.

Waiting on jobs data?

The Federal Reserve believes it has met its inflation goal and is close to its employment goal. Friday’s employment report is expected to be sufficient to allow the Fed to announce its plans to cut back on asset purchases when it meets in November.

On Wednesday, the September ADP private payroll figure exceeded expectations, boding well for the employment report, experts say. But the August gain was downwardly revised.

The 568,000 rise in payrolls in the month “is a much welcomed positive surprise,” said Steve Skancke, Keel Point chief economic advisor. But this report and the employment report have had a remarkably large divergence, “recently so whether the September jobs number … is as positive is still a question.”

The August gain was cut to 340,000 from the initially reported 374,000, which had disappointed the markets. Economists polled by IFR Markets were expecting ADP to show 430,000 new private jobs.

With government spending and the debt cap issue still to be resolved, Skancke said “there is a lot riding” on an “equally positive” jobs report.

Given recent comments by Federal Open Market Committee members, Wells Fargo Securities Senior Economist Sarah House said, “there appears to be a very low bar for a tapering announcement in November.”

And while expectations are the “jobs report will clear it,” she said, “the environment remains highly unusual, and it would not be the first time a payroll report has surprised this year.”

Wilmington Trust Chief Investment Officer Tony Roth and Chief Economist Luke Tilley said, “data suggest a further deceleration in small business hiring, suggesting some downside risks.”

With the Fed needing just a “good” report, it would take a major disappointment to derail “a potential November taper announcement,” they said.

As long as the report shows gains, the Fed will make a taper announcement in November, according to Bill Merz, director of fixed income at U.S. Bank Wealth Management.

The Fed will watch Friday’s job report to help determine whether the employment picture justifies announcing asset purchase reductions at its November meeting.

“Fed Chairman Jerome Powell clarified at the September meeting that substantial progress toward the Fed’s inflation goal has been met, and employment progress is expected to soon warrant reducing asset purchases,” Merz said. ”Other Fed officials echoed this sentiment last week, reinforcing the likelihood of an announcement in November.”

However, Grant Thornton Chief Economist Diane Swonk isn’t certain that a weak report would push back tapering. “What could stop the Fed from beginning to taper monthly purchases of Treasuries and mortgage-backed bonds? A failure to raise the debt limit before the Treasury runs out of funds to service the debt would likely force the Fed to intervene and buy Treasury bonds that the government had defaulted on.”

While forecasting a 400,000 rise in nonfarm payrolls, Scott Anderson, chief economist at Bank of the West, said the “better-than-expected private sector job gains suggest a somewhat stronger nonfarm payroll gain is possible.”

But, wage growth may be a bigger concern for the Fed, said Ned Davis Research Senior U.S. Economist Veneta Dimitrova and Chief Global Macro Strategist Joe Kalish. “Job mismatches are putting upward pressure on wage growth, particularly in lower paying industries, such as leisure and hospitality,” they said. “This may make the Fed’s job of containing inflation harder down the road.”

Consumer inflation expectations in the long term “well below short-term inflation expectations … suggests that consumers view most of the current run-up in price growth as transitory.”

The markets also see inflation returning to lower levels. “A sustained move up in inflation expectations could induce a Fed policy response, necessitating larger or more frequent rate increases, once tightening starts,” Dimitrova and Kalish said.