Municipal bonds were little changed, ignoring another reversal in U.S. Treasuries on Friday ahead of a larger-than-average $10 billion-plus calendar led by California, Texas and New York issuers.

Triple-A benchmarks were unmoved again Friday while the 10-year UST rose four basis points and the 30-year four.

As such, ratios fell slightly with the 10-year muni-to-Treasury ratio at 72% and the 30-year at 79%, according to Refinitiv MMD. The 10-year muni-to-Treasury ratio was at 72% while the 30-year was at 79%, according to ICE Data Services.

Municipals have largely decoupled from UST movements this week. Part of the reason may just be how slow secondary trading activity has been so far in September, tracking near August lows.

The past several months have turned out to be some of the slowest in terms of trading volume, noted Barclays PLC strategists in a weekly report.

“August was the lightest month in at least three years and July was not far behind. We can’t even say that low supply was responsible for this lull, as monthly issuance in July-August was close to its five-year average; we think the slowness was due to a combination of factors including rich valuations, absence of major muni-specific developments, range-bound UST rates, coupled with the vacation season,” wrote strategists Mikhail Foux, Clare Pickering and Mayur Patel.

They said activity will likely improve in the fall, as supply is expected to pick up. The Bond Buyer’s 30-day visible supply sits at $13.89 billion.

The total potential volume for the coming week is pegged at $10.671 billion, with $8.828 billion of negotiated deals led by $2 billion from California, and $1.842 billion of competitive loans, with gilt-edged issues from Maryland and Minnesota.

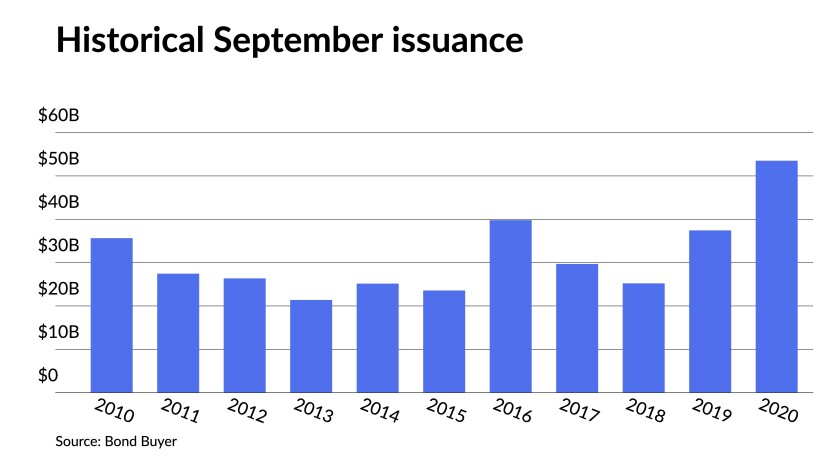

“Historically, supply in September is in the mid-30s, and this year most of it will be placed in just two to three weeks due to the extended holiday season in 2021,” they wrote.

“In our view, munis will fare relatively well, as investors have enough cash to easily absorb the pipeline, if fund flows remain supportive, and rates are in check, or even decline, responding to the softer growth data,” they said. “However, Barclays expects yields to creep higher later this year, ending the year at meaningfully higher rates compared with where we are at now.”

BofA Securities agreed in a weekly report.

“Muni rates, both tax-exempt and taxable, likely will rise in September as the infrastructure and reconciliation discussions accelerate into high gear in the second half of September,” the report said.

Secondary trading and scales

Trading was moderate for a Friday.

District of Columbia 5s of 2022 traded at 0.08%. Florida PECO 5s of 2022 at 0.08%.

Fairfax County, Virginia, 4s of 2025 at 0.30%. Wisconsin DOT 5s of 2026 at 0.42%-0.41%.

Maryland 5s of 2033 at 1.12% versus 1.10%-1.08% on Sept. 1. Maryland 5s of 2034 at 1.16% versus 1.17% Wednesday.

Out longer, New York City 5s of 2047 at 1.91% versus 1.92%-1.91% Wednesday.

Fairfax County water 4s of 2050 at 1.74%. Triborough Bridge and Tunnel 4s of 2051 at 1.87%.

Refinitiv MMD’s scale showed short yields steady at 0.08% in 2022 and 0.11% in 2023. The yield on the 10-year was steady at 0.94% while the yield on the 30-year sat at 1.53%.

The ICE municipal yield curve showed bonds steady in 2022 at 0.08% and at 0.11% in 2023. The 10-year maturity sat at 0.95% and the 30-year yield was up one to 1.53%.

The IHS Markit municipal analytics curve showed short yields steady at 0.08% and 0.11% in 2022 and 2023. The 10-year yield stayed at 0.94% and the 30-year yield sat at 1.53%.

The Bloomberg BVAL curve showed short yields steady at 0.07% and 0.07% in 2022 and 2023. The 10-year yield sat at 0.93% and the 30-year yield at 1.53%.

The 10-year Treasury was yielding 1.342% and the 30-year Treasury was yielding 1.935% in late trading. The Dow Jones Industrial Average lost 217 points or 0.62%, the S&P 500 fell 0.61% while the Nasdaq lost 0.72%.

PPI: more of the same

The producer price index came in a tick higher than expected but shouldn’t alter the Federal Reserve’s stance that inflation is transitory, although some see this as another sign tapering should begin.

Thursday’s initial claims showed an improving labor market, noted Stifel Chief Economist Lindsey Piegza. “Despite month-to-month volatility, the labor market appears on relatively solid footing,” she said. “Coupled with heightened inflation, the Fed — like the [European Central Bank] — appears to have ample justification to begin to rollback emergency measures. The question, however, is do U.S. central bankers in the U.S. have the will to begin removing the punch bowl while risks to the economy remain?”

“The strikingly high increases in the PPI for goods and services reflects a combination of strong aggregate demand fueled by excessive monetary and fiscal stimulus as well as supply constraints and bottlenecks in production processes and distribution,” said Berenberg chief economist for the U.S., Americas and Asia Mickey Levy, a member of the Shadow Open Market Committee. “Currently producers have significant flexibility to pass on increased costs to consumers; continuation of higher consumer prices will hinge on the strength of aggregate demand going forward.”

PPI grew 0.7% in August, following July’s 1.0% climb, while excluding food and energy PPI increased 0.6%, after a 1.0% rise a month earlier.

Economists polled by IFR expected the headline number to rise 0.6% and the core to fain 0.5%.

On an annualized basis, PPI rose 8.3% and ex-food and energy it climbed 6.7%. Economists expected 8.2% and 6.6% growth, respectively.

“This month’s PPI is consistent with anecdotal evidence of surging input prices, supply chain bottlenecks, and rising labor costs,” Levy said.

Strong demand and supply shortages remain “near-term challenges” that put “upward pressure on prices,” said Matt Peron, director of research at Janus Henderson Investors.

“Comments from management teams recently have indicated that the supply situation is not getting better as fast as we had hoped,” Peron said. “As a result, prices may stay elevated longer than most would like, and could stretch into 2Q next year.”

Since the numbers were close to estimates, “this is unlikely to change the Fed’s thinking,” he said. “And with housing softening a bit, they are likely to let the supply chain issues play out in the next few months.”

While the economy continues to run “a little hot,” as expected, Peron said, “nothing in the release will move them off the base case ‘transitory’ narrative.”

Also released Friday, wholesale inventories grew 0.6% in July, as expected by economists, after a 1.2% jump in June, while wholesale sales rose 2.0% after a 2.3% climb in June.

Primary to come

California (Aa2/AA-/AA/) is set to price on Monday for retail investors $2.092 billion of general obligation bonds, consisting of Series 1 $1.04 billion and Series 2 $1.051 billion. Morgan Stanley & Co. LLC.

The Black Belt Energy Gas District (A2///) is set to price on Wednesday $805.325 million of gas project revenue bonds, 2021 Series B. Goldman Sachs & Co. LLC.

Providence St. Joseph Health Obligated Group (Aa3/AA-/AA-/) is set to price on Tuesday $775 million of taxable bonds, Series 2021A. Goldman Sachs & Co. LLC.

The Long Island Power Authority (A2/A/A/) is set to price on Tuesday $737.74 million of electric system general revenue bonds, Series 2021, consisting of $368.25 million of Series 21A, serials 2022-2042; $175 million of mandatory tender bonds, Series 21B, serial 2051; and $194.49 million of taxable of Series 21C, serial 2023. Wells Fargo Corporate & Investment Banking.

The New York City Municipal Water Finance Authority (Aa1/AA+/AA+/) is set to price on Tuesday $633 million of water and sewer system second general resolution revenue bonds, Fiscal 2022 Series BB, consisting of: $545 million, Series BB-1, serials 2039, 2044-2045, and $88 million, Series BB-2, serial 2027. Raymond James & Associates.

The North Texas Higher Education Authority, Inc. is set to price $478 million of taxable student loan asset-backed notes, Series 2021-1, consisting of $118 million Series A-1A (/AA+//), $350 million Series A-1B (/AA+//), and $10 million Series 21-1B (/AA//). BofA Securities.

Illinois (/BBB+/BBB+/AA+) is set to price on Wednesday $400 million of Build Illinois Bonds sales tax revenue bonds, junior obligation taxable Series B and junior obligation tax-exempt refunding Series C. Ramirez & Co., Inc.

Atlanta (Aa3//AA-/) is set to price on Tuesday airport general revenue refunding bonds, consisting of: $45.145 million, Series 2021A (non-AMT), serials 2022-2042; $132.455 million, Series 2021B (non-AMT), serials 2022-2042; and $164.11 million, Series2021C (AMT), serials 2022-2042. Loop Capital Markets.

The Texas Transportation Commission (Aaa/AAA/AAA/) is set to price on Thursday $250 million of State of Texas general obligation mobility fund put bonds, Series 2014-B. Wells Fargo Corporate & Investment Banking.

Texas (Aaa/AAA/AAA/) is set to price on Wednesday $209.285 million of general obligation bonds, consisting of $29.03 million of water financial assistance bonds, Series 2021A, serials 2022-2046; $164.435 million of water financial assistance refunding bonds, Series 2021B, serials 2022-2038; and $15.815 million of water financial assistance refunding bonds (Economically Distressed Areas Program), Series 2021, serials 2022-2029. Raymond James & Associates, Inc.

The Washington Health Care Facilities Authority (Aa3/AA-/AA-/NR) is set to price on Tuesday $192.755 million of refunding revenue bonds, Series 2021B. Morgan Stanley & Co. LLC.

The Kentucky Public Transportation Infrastructure Authority (A2/AA//AA+) is set to price $191.81 million of taxable first tier toll revenue bonds (Downtown Crossing Project), Series 2021A, insured by Assured Guaranty Municipal Corp., serials 2021, 2025-2033, terms 2039, 2049, 2053. Citigroup Global Markets Inc.

The East Whittier City School District, Los Angeles County, California, (Aa2///) is set to price $180 million of election of 2016 general obligation bonds, Series D. RBC Capital Markets.

The Mt. Diablo Unified School District, California (Aa3///) is set to price on Thursday $170 million of refunding and forward deliver bonds. Stifel, Nicolaus & Company, Inc.

The State of Connecticut Health and Educational Facilities Authority (A2/A/A+/) is set to price $167.365 million of Hartford Healthcare revenue bonds, serials 2025-2041, terms 2046, 2051, on Tuesday. Citigroup Global Markets Inc.

The Connecticut Housing Finance Authority (Aaa/AAA//) is set to price on Tuesday $161.205 million of housing mortgage finance program social bonds. Morgan Stanley & Co. LLC.

The Milpitas Unified School District, California (Aa1/AA//) is set to price on Tuesday $150 million of general obligation bonds, serials 2022-2041, term 2046. Citigroup Global Markets Inc.

The City of Farmington, New Mexico (Baa2/BBB//) is set to price on Wednesday $146 million of pollution control revenue refunding bonds (Public Service Company of New Mexico San Juan and Four Corners Projects). U.S. Bancorp Investments Inc.

The Nebraska Public Power District (A1/A+/A+/) is set to price on Tuesday $138.845 million of general revenue bonds. Goldman Sachs & Co. LLC.

The California Municipal Finance Authority (//A-/) is set to price on Thursday $120 million of HumanGood senior living revenue bonds. Ziegler

Competitive

The Massachusetts School Building Authority (Aa3/AA/AA+) is set to sell $344.335 million of taxable subordinated dedicated sales tax refunding bonds, 2021 Series A at 10 a.m. eastern on Tuesday.

Hennepin County, Minnesota, (/AAA/AAA) is set to sell $100 million of general obligation bonds, Series 2021A at 11:30 a.m. Tuesday.

Austin, Texas, (-/-/AA+) is set to sell $20.38 million of certificates of obligation, taxable series 2021 taxable, at 11:30 a.m. Tuesday.

Austin (-/-/AA+) is set to sell $29.425 million of public property finance contractual obligations, Series 2021, at 10:30 a.m. Tuesday.

Austin (-/-/AA+) is set to sell $36.535 million of certificates of obligation, Series 2021, at 10:30 a.m. Tuesday.

Austin (-/-/AA+) is set to sell $83.655 million of public improvement and refunding bonds, Taxable Series 2021 Taxable, at 11:30 a.m. Tuesday.

Austin (-/-/AA+) is set to sell $163.095 million of public improvement and refunding bonds, Series 2021, at 10:30 a.m. Tuesday.

Frederick County, Maryland, (Aaa/AAA/AAA) is set to sell $30.91 million of general obligation public facilities taxable refunding bonds, Series 2021B taxable, at 10:30 a.m. Tuesday.

Frederick County (Aaa/AAA/AAA) is set to sell $150.5 million of general obligation public facilities taxable refunding bonds, Series 2021A, at 10:15 a.m. Tuesday.

Greenville, Texas, (-/AA-/-) is set to sell $54.5 million of general obligation bonds, Series 2021, at 10 a.m. Tuesday.

Greenville (-/AA-/-) is set to sell $67.625 million of combined tax and revenue certificates of obligation, Series 2021, at 10 a.m. Tuesday.

The Mt. Diablo Unified School District, California, (Aa3///) is set to price on Thursday $170 million of refunding and forward delivery bonds. Stifel, Nicolaus & Company, Inc.

The State of Connecticut Health and Educational Facilities Authority (A2/A/A+/) is set to price $167.365 million of Hartford Healthcare revenue bonds, serials 2025-2041, terms 2046, 2051, on Tuesday. Citigroup Global Markets Inc.

The Connecticut Housing Finance Authority (Aaa/AAA//) is set to price on Tuesday $161.205 million of housing mortgage finance program social bonds. Morgan Stanley & Co. LLC.

The Milpitas Unified School District, California, (Aa1/AA//) is set to price on Tuesday $150 million of general obligation bonds, serials 2022-2041, term 2046. Citigroup Global Markets Inc.

The City of Farmington, New Mexico, (Baa2/BBB//) is set to price on Wednesday $146 million of pollution control revenue refunding bonds (Public Service Company of New Mexico San Juan and Four Corners Projects). U.S. Bancorp Investments Inc.

The Nebraska Public Power District (A1/A+/A+/) is set to price on Tuesday $138.845 million of general revenue bonds. Goldman Sachs & Co. LLC.

The California Municipal Finance Authority (//A-/) is set to price on Thursday $120 million of HumanGood senior living revenue bonds. Ziegler.

Jessica Lerner contributed to this report.