The municipal market was little changed on Friday as a disappointing August jobs number punctuated an otherwise lackluster day of light trading activity ahead of the Labor Day holiday.

Trading fell to a trickle at about $2.1 billion near the close and triple-A benchmarks were unmoved, outperforming a cheaper U.S. Treasury market which saw the 10- and 30-year yield rise four and five basis points, respectively, while equities were mixed.

Ratios fell slightly with the municipal to UST 10-year ratio at 70% and the 30-year at 78%, per Refinitiv MMD. The 10-year muni-to-Treasury ratio was at 72% and the 30-year was at 78%, according to ICE Data Services.

“Munis are holding up better than their taxable counterparts today, but on track for a down week and a continuation of August themes here in early September,” Anthony Valeri, director of investment management at Zions Wealth Management said Friday.

“Today’s better resilience of munis relative to high-quality taxable bonds shouldn’t offset what looks to be another week of muni underperformance relative to Treasuries,” he said.

Additionally, dealers may be hedging or preparing for next week’s slate of Treasury auctions, he said, pointing to the approximately $133 billion being auctioned in Treasury notes and bills next week.

“The market remains well bid before the holiday,” John Mousseau, president and director of fixed income at Cumberland Advisors said Friday. “Treasuries are off even with a jobs number below expectations as June and July were revised up and unemployment dropped 0.2%.”

The new-issue calendar totals $5.987 billion, according to Ipreo and The Bond Buyer, down from total revised volume of $3.648 billion, according to Refinitiv.

Competitive sales next week are estimated at $1.869 billion, down from $1.034 billion, while

negotiated sales are estimated at $4.118 billion, down from $2.614 billion.

The negotiated calendar is led by a $1 billion taxable healthcare deal from Piedmont Healthcare, Inc., Georgia (A1/AA-//), an $800 million-plus transportation notes deal from Hampton Roads, Virginia and a $500 million non-rated senior living project from Texas.

Triple-A-rated Minnesota leads the competitive calendar with $879.1 million of general obligation and trunk highway bonds on Thursday.

Municipal supply is still lagging demand with Bond Buyer 30-day visible supply at $10.30 billion, while Bloomberg shows net negative supply at $11.430 billion.

“With four months remaining in the year, we remain sanguine on the performance trajectory for munis as we continue to see new-issue supply unable to keep pace with bond redemptions and maturing securities,” said Jeff Lipton, head of municipal credit and market strategy and municipal capital markets at Oppenheimer & Co.

“Although we believe that munis still have the ability to generate positive performance, admittedly such performance could be compromised should technicals become much less constructive and prospects for higher taxes fade considerably, even from currently elevated levels of doubt,” he said.

Refinitiv Lipper reported a slowing down of all inflows this week — albeit still above $1 billion — giving some investors pause.

“Should there be sustained market disruption in the pace and/or direction of municipal fund flows with a market correction of material consequence given the currently low base level of yields, the muni high-yield sector could see a more pronounced widening-out in spreads (perhaps brought about by a credit event),” Lipton added.

High-yield municipals posted a 0.16% loss in August, the first since the major disruption from COVID in spring 2020, but 2021’s gain sits at 7.23%.

Lipton noted high-yield investors should consider underlying risks.

“While value can be found with acquiring high-yield securities, high-yield investors should exercise care when seeking alpha, as various credits are being structured with weaker covenants,” Lipton said. “We believe that tightly secured covenants are of particular benefit in a contractionary period whereby revenue disruption could occur.”

Just late last month, Nuveen filed a soft close of two of its high-yield bond funds, which some participants see as a signal that high-yield might be overbaked.

“After careful consideration, Nuveen has decided to soft close all share classes of the Nuveen High Yield Municipal Bond Fund (NHMRX) and Nuveen California High Yield Municipal Bond Fund (NCHRX) to new investors effective September 30th,” a spokesperson said. “Nuveen investment and product teams will closely monitor market conditions and other fund-specific factors and will actively look to reopen the funds when it is deemed to be in the best interest of shareholders.”

The funds will continue to accept purchases from existing shareholders. The firm said it believes regulating asset growth through a soft closing “is currently in the funds’ shareholders best interest.”

Secondary market

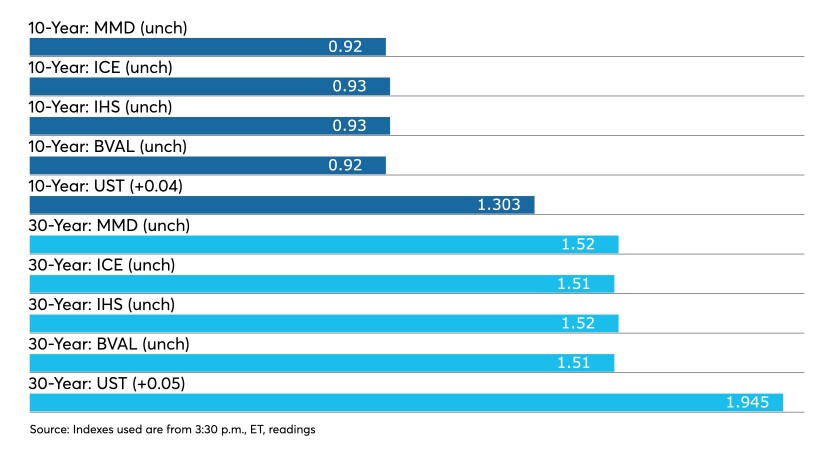

Short yields were steady at 0.08% in 2022 and 0.11% in 2023 on Refinitiv MMD’s scale. The yield on the 10-year at 0.93% while the yield on the 30-year sat at 1.52%.

The ICE municipal yield curve showed bonds steady in 2022 at 0.08% and 0.11% in 2023. The 10-year maturity sat at 0.94% and the 30-year yield 1.51%.

The IHS Markit municipal analytics curve showed short yields steady at 0.08% and 0.10% in 2022 and 2023. The 10-year yield stayed at 0.93% and the 30-year yield held steady at 1.52%.

The Bloomberg BVAL curve showed short yields steady at 0.07% and 0.07% in 2022 and 2023. The 10-year yield stayed at 0.92% and the 30-year yield at 1.51%.

The 10-year Treasury was yielding 1.323% and the 30-year Treasury was yielding 1.945% in late trading. The Dow Jones Industrial Average lost 58 points or 0.16%, the S&P 500 fell 0.01% while the Nasdaq gained 0.18%.

Employment report disappoints

“Taper is dead … for now,” said Bryce Doty, senior portfolio manager at Sit Investment Associates, after the employment report came in well short of expectations. “This gives Jay Powell an excuse to push off tapering until his reappointment as Fed Chair in February.”

The report was a key piece of information that could change the Federal Reserve’s timing on making a tapering announcement. Powell has said there needs to be “substantial further progress” on the employment goal before it will cut back on asset purchases.

That time is “still at least a month or two away,” said Fitch Ratings Chief Economist Brian Coulton.

While this probably won’t “alter the Fed’s intention to taper before the end of the year,” said Scott Anderson, chief economist at Bank of the West, “it does probably keep the Fed data dependent at the September FOMC meeting as they await a few more employment reports before going ahead with the reduction in monthly asset purchases.”

The miss “should reinforce the Fed’s wait-and-see approach,” noted Sameer Samana, senior global market strategist, Wells Fargo Investment Institute.

“Fed officials were eagerly awaiting this report and now the hawks will need to wait to see more data,” said Ed Moya, senior market analyst for the Americas at OANDA.

Some felt the report would give a clearer picture of how the Delta variant is impacting the economy. But there is no clear agreement on that, either.

“This job data cannot be blamed on the Delta variant,” Doty said.

However, Jack Janasiewicz, senior vice president, portfolio manager and portfolio strategist at Natixis Investment Managers Solutions, said, “it has the Delta variant written all over it.”

Still, not only did Delta have “apparent” impacts on hiring and the economy, said Dana M. Peterson, chief economist at The Conference Board, “Looking forward, the ongoing increase in the number of new infections is likely to lead to another subpar payrolls print in September.”

Non-farm payrolls rose 235,000 in August after an upwardly revised 1.053 million in July, first reported as 943,000.

Economists polled by IFR Markets expected 728,000 jobs to be added in the month.

The upward revisions for July and June “doesn’t make a dent in the disappointing data,” Sit’s Doty said. “There is a near record number of job openings and yet so few jobs” added, he said.

Besides the $300 added unemployment benefits, Doty said, “Once people have gotten a taste for working remotely, it’s hard to give that up and employers’ requiring people to come back into the office has fueled a wave of resignations, creating a headwind for job growth.”

Despite the lower-than-expected read, Fitch’s Coulton said, nonfarm payrolls have grown an average of 750,000 in the past three months, and “the level of employment is now only 3.5% below pre-virus levels.”

Noting leisure and hospitality, which had been hiring, saw a “halt in job growth” this month, might suggest “an impact from the surge in virus cases on the pace of reopening.”

The labor market is recovering, Wells Fargo’s Samana said, as shown by lower unemployment and underemployment rates.

“Wage growth was another bright spot,” he said, “and shows that employees have bargaining power against employers.”

Average hourly earnings grew 0.6% in August, after a 0.4% gain in July. But average weekly hours remained at 34.7 “and will need to be monitored,” Samana said.

The labor participation rate holding at 61.7% “will disappoint Fed hawks that were looking to claim further that the labor market recovery is now delivering further substantial progress,” OANDA’s Moya said.

Also released Friday, the Institute for Supply Management’s services survey showed growth was slower than in July, while prices remained high, but softened and employment was growing at a steady pace.

The services PMI fell to 61.7 in August from 64.1 in July. Economists expected a 61.8 read.

Primary to come

Piedmont Healthcare, Inc., Georgia (A1/AA-//) is set to price $1 billion of taxable bonds on Thursday, serials 2032, 2042, 2052. RBC Capital Markets.

The Hampton Roads Transportation Accountability Commission (Aa2/A+//) is set to price on Thursday $817.99 million of Hampton Roads Transportation Fund senior lien bond anticipation notes, serial 2026. Citigroup Global Markets Inc.

The New Hope Cultural Education Facilities Finance Corp., Texas, (nonrated) is set to price $498.865 million of Sanctuary LTC project senior living revenue bonds on Thursday, consisting of: $413.515 million of Series S21A1, serials 2025-2057; $16.95 million Series S21A2, serials 2022-2025; and $53 million of Series S21B, serials 2022-2057. HilltopSecurities.

Grand Forks, North Dakota (Baa2//BBB-/) is set to price on Wednesday $382.635 million of Altru Health System fixed rate bonds. BofA Securities.

The Windler Public Improvement Authority, Colorado (nonrated) is set to price $291.326 million of Limited Tax Supported Revenue Bonds, Series 2021A-1, $210.11 million and $81.216 million of Limited Tax Supported Convertible Capital Appreciation Revenue Bonds, Series 2021A-2. Piper Sandler & Co.

The CSCDA Community Improvement Authority (nonrated) is set to price on Wednesday $230.95 million of essential housing social revenue bonds (Orange Portfolio), consisting of $75 million of Series A-1, serial 2047, and $105.2 million, Series A-2, serial 2057, and $50.75 million of Series B, serial 2057. Goldman Sachs & Co. LLC.

The West Harris County Regional Water Authority, Texas (A1/AA/AA-/) is set to price $188 million of water system revenue and revenue refunding bonds, Series 2021, insured by Build America Mutual, serials 2032-2041, terms 2046, 2051, 2060. Jefferies LLC.

The Minnesota Housing Finance Agency (Aa1/AA+//) is set to price on Thursday $150 million of residential housing finance bonds, Series E AMT social bonds and Series F, non-AMT social bonds. RBC Capital Markets.

The Illinois Housing Development Authority (Aaa///) is set to price on Thursday $144.3 million of exempt and taxable social revenue bonds. J.P. Morgan Securities LLC.

The Michigan Strategic Fund (Ba2/BB//) is set to price on Thursday $100 million of variable rate limited obligation revenue green bonds (Graphic Packaging International, LLC Coated Recycled Board Machine Project), serial 2061. TD Securities LLC

Competitive deals

Minnesota (/AAA//) is set to sell $311 million of unlimited tax general obligation bonds at 10:30 a.m. eastern, $284.1 million of ULT GOs at 11 a.m. and $284 million at 11:30 a.m. Thursday.

The Dublin USD, California is set to sell $116 million of general obligation bonds at 12:30 p.m. eastern on Thursday.

Athens Clarke County USD, Georgia (/AA//) is set to sell $93.175 million of unlimited tax general obligation bonds at noon Thursday.