Municipal benchmark yields rose by as much as five basis points Friday, following a stronger-than-expected jobs report, but the asset class outperformed the moves in Treasury bonds. An increase in supply next week may test current low levels.

Continued strength in the economy was seen as nonfarm payrolls rose 943,000 and the jobless rate fell to 5.4% last month, the Labor Department reported.

“The dollar is surging following a better-than-expected nonfarm payroll report, which may have paved the way for the Fed to announce tapering if the economy delivers one more robust report in September,” said Ed Moya, senior market analyst for the Americas at OANDA. “The steepener trade is back as Treasury yields soar higher. The 10-year Treasury yield seems destined for 1.30%, with further upside likely targeting 1.35% over the next week or two.”

The 10-year UST was trading at 1.30% and the 30-year at 1.940% at the close. High-grade benchmark yields rose three to five basis points on 10-year while the 10-year Treasury yield rose eight basis points and the muni 30-year rose two to four basis points while the 30-year was up nine.

As such, ratios were at 67% in 10 years and 73% in 30, according to Refinitiv MMD while ICE Data Services had the 10-year at 68% and the 30 at 72%.

Much of muni performance will depend on UST performance. While municipals lagged Friday’s UST moves, they may play catch up with the increase in issuance next week along with large UST auctions.

Supply ticks up next week with the total potential volume at $7.677 billion. There are $6.162 billion of negotiated deals on tap and $1.514 billion of competitive loans. Thirty-day visible supply sits at $9.96 billion, according to Bond Buyer data.

Gilt-edged Maryland has $615 million of exempt and taxable unlimited tax general obligation bonds in three sales Wednesday.

The Massachusetts Bay Transportation Authority (Aa3/AA//) is set to sell $328 million of subordinate sales tax sustainability bond anticipation notes Tuesday.

In the negotiated market, the Allegheny County Airport Authority (A2//A/A+) leads the slate with $823.55 million of Pittsburgh International Airport AMT and non-AMT revenue bonds on Wednesday.

“Tax-exempt supply is still expected to be quite manageable, fund inflows are robust (although their pace has noticeably declined somewhat), but more importantly net issuance in August should be close to minus $15 billion, including the coupons,” Barclays strategists said in a weekly report.

Visible supply for taxable municipals has “declined to one of its lowest levels this year, as high-quality taxables have underperformed similar-rated corporates,” the Barclays report said.

“We see value in AAA and high-AA munis at current levels, as demand from life insurers will likely improve in the aftermath of changes in the NAIC risk-weightings,” according to Barclays.

“BBBs have been steadily outperforming corporates, propelled by credits in the Illinois complex. There are still some opportunities in the BBB bucket, but they are few and far between,” they said.

BofA Securities said in its weekly report that high-yield and BBB-rated bonds “not only performed best year-to-date, but we believe should continue to offer the best additional performance from here through year-end, especially the longer part of the curve.”

High-grade investors should move to lower coupons and extend their portfolio durations, BofA strategists Yingchen Li and Ian Rogow said.

“Our coupon performance reviews shows that 4% coupons have been performing the bet across the board while 3% coupons have lagged, especially in the AAA space,” they wrote. “High-grade investors should focus on 3% coupons going forward to improve portfolio performance.”

While Friday’s jobs data was positive, the Delta variant threat remains. “It was nice to get some good news on jobs after rather disheartening headlines around COVID continue, but the market should keep those in mind before the bears start digging in,” a New York trader said. “We are starting to see the increased measures being put into place (masks and vaccine mandates) which to my mind, does not put me at ease on a continued robust economic pace.”

Secondary trading and scales

Trading showed yields climbing across the curve. California 5s of 2024 at 0.15%. Montgomery County, Maryland 4s of 2025 at 0.22%. Florida BOE PECOs 5s of 2025 at 0.24%. New York Dorm PITs 5s of 2026 at 0.33%. New York UDC 5s of 2026 at 0.37%.

Wisconsin 5s of 2028 at 0.62%. Montgomery County 4s of 2029 at 0.79%.

Maryland 5s of 2032 at 0.95% versus 0.89%-0.88% Thursday. Michigan trunkline 5s of 2034 at 1.25%-1.24% versus 1.17% Thursday and 1.20% original.

Washington 5s of 2041 at 1.42% versus 1.39%-1.31% Thursday. Georgia road and tollway 4s of 2044 at 1.47%-1.36%.

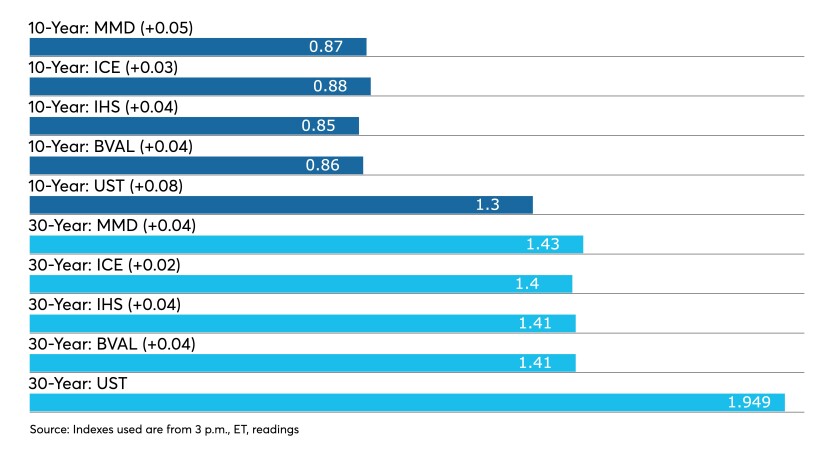

Refinitiv MMD had yields rose three basis points to 0.08% in 2022 and to 0.08% in 2023. The yield on the 10-year rose five to 0.87% while the yield on the 30-year rose four to 1.43%.

ICE municipal yield curve saw bonds rise to 0.05% in 2022 (+1) and to 0.06% in 2023 (+1). The 10-year maturity rose three to 0.88% and the 30-year yield up two to 1.41%.

The IHS Markit municipal analytics curve saw the one-year rise two to 0.07% and the two-year to 0.08%, with the 10-year up four basis points to 0.85%, and the 30-year yield up four to 1.41%.

Bloomberg BVAL saw levels rise to 0.04% (+1) in 2022 and 0.05% (+2) in 2023, while the 10-year rose four to 0.86% and the 30-year up four to 1.41%.

Treasuries were higher while equities were mixed. The 10-year Treasury was yielding 1.30% and the 30-year Treasury was yielding 1.859% in late trading. The Dow Jones Industrial Average rose 110 points or 0.32%, the S&P 500 gained 0.08% while the Nasdaq lost 0.48%.

Strong jobs report eases pressure on the Fed

The U.S. economy gained more jobs than expected in July, continuing its strong rebound while the employment rate fell, news economists said could let the Federal Reserve begin tapering as early as this year.

Nonfarm payrolls rose 943,000 in July as the jobless rate fell to 5.4% from 5.9% in June, the Labor Department reported.

Economists surveyed by IFR Markets had expected payrolls to have risen by 900,000 and the jobless rate to dip to 5.7%.

June’s number was upwardly revised to show a gain of 938,000 jobs, originally reported as an increase of 850,000.

The Labor Department noted large job gains were seen last month in the leisure and hospitality sectors and in local government education.

“Job creation is now surprising on the upside, with payroll gains averaging over 800,000 per month since May,” said Brian Coulton, chief economist at Fitch Ratings. “The employment to population ratio rose by 0.4 percentage points in July, the biggest one month jump since last October, helped by large gains in hiring in leisure and hospitality.”

He said the strong report could spur the Fed to act.

“If we get another print of near 1 million payroll gains for August, it’s possible that the Fed could start to view the progress being made in labor market recovery as being ‘substantial,’ Coulton said. “With clearer evidence of wage growth picking up, the tapering of Fed asset purchases is looking more and more likely to happen this year now.”

Other economists agreed.

“Labor market conditions in July show that more and more people are getting back to work, working longer and earning somewhat more,” said Christian Scherrmann, DWS Group’s U.S. Economist. “Today’s upside surprise should strengthen the confidence in labor market recovery and brings the Fed just another step closer to declaring ‘sufficient further progress’ — something that we see as likely in September.”

Some noted the continued strength in the economy.

“Coming on the heels of June’s already strong numbers, which were also revised higher, that now makes two months in a row of close to 1 million jobs created,” said Sameer Samana, senior global market strategist at Wells Fargo Investment Institute. “This reinforces our view that the labor market is on solid footing and will be the main driver of economic growth (via consumption). It also keeps the Fed on track to taper bond purchases towards the end of 2021/beginning of 2023, which should put upward pressure on long-term interest rates.”

The decline in the unemployment rate came as the number of unemployed persons fell 782,000 to 8.7 million.

“These measures are down considerably from their highs at the end of the February-April 2020 recession,” the Labor Department said.

However, it noted the remained well above their pre-COVID-19 pandemic levels of 3.5% and 5.7 million in February 2020.

In July, employment in leisure and hospitality increased by 380,000, with two-thirds of the gains being in food services and drinking establishments. Employment also continued to increase in accommodation and in arts, entertainment and recreation.

Despite the growth, employment in leisure and hospitality is down 10.3%, or by 1.7 million, from February 2020 levels.

Employment rose 221,000 in local government education and by 40,000 in private education. Since February 2020, employment is down by 205,000 in local government education and by 207,000 in private education.

“The fact the US economy is bubbling away and ready for a period of expansion is now the worst kept secret in global markets,” said Erez Katz, CEO of Neuravest Research. “July’s data has just poured a whole lot more fuel on the fire for inflation hawks as legions of workers who were previously inactive return to take up jobs in sectors now finding their feet again, particularly in the leisure and hospitality industries.”

The size of the U.S. force has been holding steady, so it appears July’s gains were driven by unemployed workers looking for and finding jobs.

“Recent weeks have seen large drops in workers on unemployment rolls, particularly in the states that have ended participation in the enhanced federal unemployment benefits,” said Noah Williams, adjunct fellow at Manhattan Institute, and Juli Plant Grainger, professor of economics at the University of Wisconsin, Madison.

However, they said the trends of growth in food services and education employment are threatened by the increased virus spread with the Delta variant and re-imposed public health restrictions in response.

“September had looked to mark a larger upturn in the economy, with the full expiration of unemployment benefits and the return to schooling and easing of childcare pressures. But that upturn is now in doubt,” they said.

“The jobs report was excellent,” said Nancy Tengler, Chief Investment Officer of Laffer Tengler Investments. “I believe part of the reason is the cessation of supplemental benefits in many states. I split my time between Nevada and Arizona. Arizona stopped the benefits on July 10 — not a help wanted sign anywhere. In Incline Village in Nevada virtually every establishment has a help wanted sign in the window — gas stations, grocery store, post office, pet store, coffee shop, you name it. Supplemental benefits are still in place.”

In July, 13.2% of employed persons teleworked because of the coronavirus pandemic, down from 14.4% in the prior month. These data refer to employed persons who teleworked or worked at home specifically because of the pandemic.

Additionally, some say inflation may be finally making its big return.

“Advancing wage growth capable of rapidly firing up consumer spending is making it increasingly likely the central bank will need to respond sooner rather than later,” Katz said. “Those proclaiming that soaring inflation is temporary will continue to shift uncomfortably in their chairs. Nowhere is inflation straining at the leash quite like in the U.S., a powerhouse of an economy that still has the power to set the agenda that others follow.”

Primary to come

In the competitive market, the Massachusetts Bay Transportation Authority (Aa3/AA//) is set to sell $328 million of subordinate sales tax sustainability bond anticipation notes at 10:45 a.m. Tuesday.

Gilt-edged Maryland has $615 million of exempt and taxable unlimited tax general obligation bonds in three sales Wednesday: $258.95 million at 10 a.m. eastern, $281.05 million at 10:30 a.m. and $75 million of taxables at 11.

In the negotiated market:

The Allegheny County Airport Authority (A2//A/A+) is set to price $823.55 million of Pittsburgh International Airport AMT and non-AMT revenue bonds on Wednesday. $711.13 million AMT, Serials 2026-2041, terms 2046, 2051, 2056; and $112.42 million non-AMT, Serials 2026-2041; terms 2046, 2051, 2056. Citigroup Global Markets Inc.

The Triborough Bridge and Tunnel Authority is set to price on Thursday $450 million of MTA Bridges and Tunnels payroll mobility tax senior lien bonds. J.P. Morgan Securities LLC.

The New York City Housing Development Corp. (Aa2/AA+//) is set to price on Wednesday $310.375 million of Multi-Family Housing Revenue Bonds, 2021 Series G-1 (Non-AMT) (Sustainable Development Bonds), 2021 Series G-2 (AMT) (Sustainable Development Bonds). Morgan Stanley & Co. LLC, New York

The City of Lubbock, Texas (A1/A+/A+/) is set to price on Thursday $254.32 million of electric light and power system revenue bonds. BofA Securities.

Maryland (Aaa/AAA/AAA/) is set to price on Tuesday $237.625 million of general obligation forward-delivery refunding bonds. BofA Securities.

The CSCDA Community Improvement Authority, California (nonrated) is set to price on Wednesday $236.565 million of essential housing revenue social bonds, serials 2057. Goldman Sachs & Co. LLC.

The City of San Antonio, Texas (Aaa/AAA/AA+/) is set to price $226.53 million of general improvement bonds, combination tax and revenue certificates of participation and taxable combination tax and revenue certificates of obligation. J.P. Morgan Securities LLC.

The Oregon Community College Districts (/AA//) is set to price on Wednesday $214.235 million of full faith and credit pension obligations. Piper Sandler & Co.

The Henry County School District, Georgia (Aa1/AA+//) is set to price $210 million of general obligation bonds (Insured by: Georgia State Aid Intercept Program), serials, 2024-2036. Raymond James & Associates, Inc.

The Del Valle Independent School District, Texas (/AAA//) (PSF Guarantee) is set to price on Tuesday $187.275 million of unlimited tax school building bonds, serials 2022-2041. Siebert Williams Shank & Co., LLC.

The Bastrop Independent School District, Texas (Aaa/AAA//) (PSF Guarantee) is set to price $170.395 million of unlimited tax school building bonds and refunding bonds. Piper Sandler & Co.

The Windy Gap Firming Project Water Activity Enterprise, Colorado (Aa2/AA//) is set to price on Thursday $165.665 million of Windy Gap Firming Project senior revenue bonds. Goldman Sachs & Co. LLC.

The Allentown Neighborhood Improvement Zone Development Authority (Baa3///) is set to price on Tuesday $159.595 million of forward delivery tax revenue refunding bonds, serials 2024-2036, term 2042. Citigroup Global Markets Inc.

The City of Garland, Texas (A1//AA-/) is set to price on Tuesday $152.825 million of electric utility system taxable revenue refunding bonds. BofA Securities.

The Virginia Housing Development Authority (Aaa/AAA//) is set to price $151.129 million of commonwealth mortgage bonds, residential mortgage-backed securities, serial 2051. Wells Fargo Corporate & Investment Banking.

Friendship Independent School District, Texas (Aaa/AAA//) (PSF Guarantee) is set to price on Tuesday $141 million of unlimited tax school building bonds, serials, 2022-2024, 2034-2051. RBC Capital Markets.

The University of North Dakota is set to price on Thursday $130.4 million of certificates of participation. Stifel, Nicolaus & Company, Inc.

Pecos-Barstow-Toyah Independent School District (/AAA//) (PSF Guarantee) is set to price on Wednesday $111.79 million of unlimited tax school building bonds, serials 2022-2041. RBC Capital Markets.